Most traders do not fail prop evaluations because they cannot read a chart. They fail because they bring a personal-account strategy into a rule-heavy environment and only notice the mismatch after the damage is done.

At first, that mismatch barely looks like a problem. Two normal losses. A recovery trade sized a little too large. A strong winner that retraces too far under a trailing drawdown model. A setup that works best during news, traded in an account that restricts news exposure. None of this is unusual. It is ordinary trading behavior colliding with a very specific rulebook.

That is the real shift: in prop trading, the rules are not wrapped around your strategy. They are part of the strategy. If your method cannot survive max daily loss, trailing drawdown, timing restrictions, and consistency rules, it is not prop-firm-ready no matter how good the entry looks.

This guide is about adapting an existing edge so it can survive long enough to reach payouts. Not pass fast. Survive first.

Prop Firm Rules Do Not Sit Around Your Strategy. They Define It.

A lot of prop content treats rules like admin details. Learn the numbers, avoid violations, move on.

That misses the point.

A prop challenge is not just testing whether you can make money. It is testing whether you can operate inside external constraints without losing control. That changes what counts as a viable strategy.

Why good traders still fail evaluations

A trader can be directionally right and still fail the challenge.

Imagine someone with a solid intraday breakout setup. In a personal account, they risk 1% per trade, take three to five attempts a day, and sometimes press size after an early loss when volatility expands. That may be messy, but it can survive in a flexible environment.

Put the same behavior inside a tight prop structure and it becomes fragile fast. Two losses can consume most of the day’s room. A third trade is no longer just another attempt. It is a rule event. If the trader responds by increasing size to make the day back, the account often dies at the point where chart-reading matters least.

The setup was not necessarily the problem. The architecture was.

The difference between trading edge and rule-compatible edge

A useful distinction:

- Trading edge means your method has positive expectancy.

- Rule-compatible edge means that expectancy can survive the firm’s limits long enough to matter.

Those are not the same.

A strategy can work in a personal account and still fail in a prop account because the loss distribution is too lumpy, the holding style clashes with drawdown rules, or the best setups occur during restricted news windows.

That is why “best prop firm strategy” is usually the wrong question. The better one is: which parts of my current strategy become dangerous once the rulebook becomes part of market structure?

The Three Rules That Change Strategy Design Most

Not every firm uses the same rules, and the exact calculations vary by firm and account type. You should always verify the current official rulebook before trading.[^1]

Still, three constraints do most of the damage in practice.

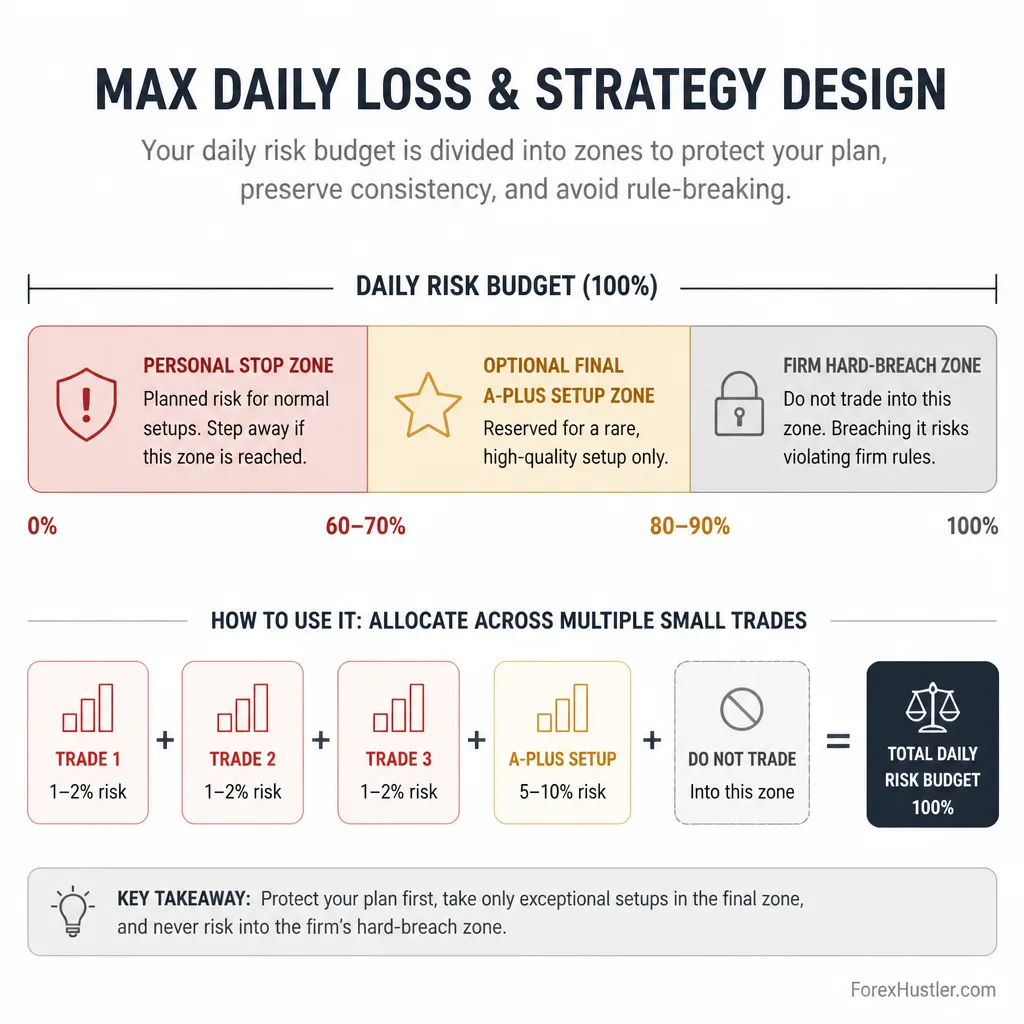

Max daily loss: the rule that kills revenge trading and oversized recovery

Max daily loss is the largest loss you can take in a trading day before breaching the account. Firms do not all calculate it the same way. Some reference start-of-day balance, some previous end-of-day balance, and some include current equity.[^2]

Strategically, the point is simpler: it limits how many mistakes you can make before the day is over.

Here is the trap. If your account has a tight daily loss cap and you risk 1% per trade, two normal losses, plus spread and slippage, can leave you with almost no room. At that point, even a valid third setup becomes dangerous because decision quality usually gets worse when available rule room gets small.

This is why daily loss rules punish recovery behavior. They are designed to stop a manageable red day from turning into an account-ending one.

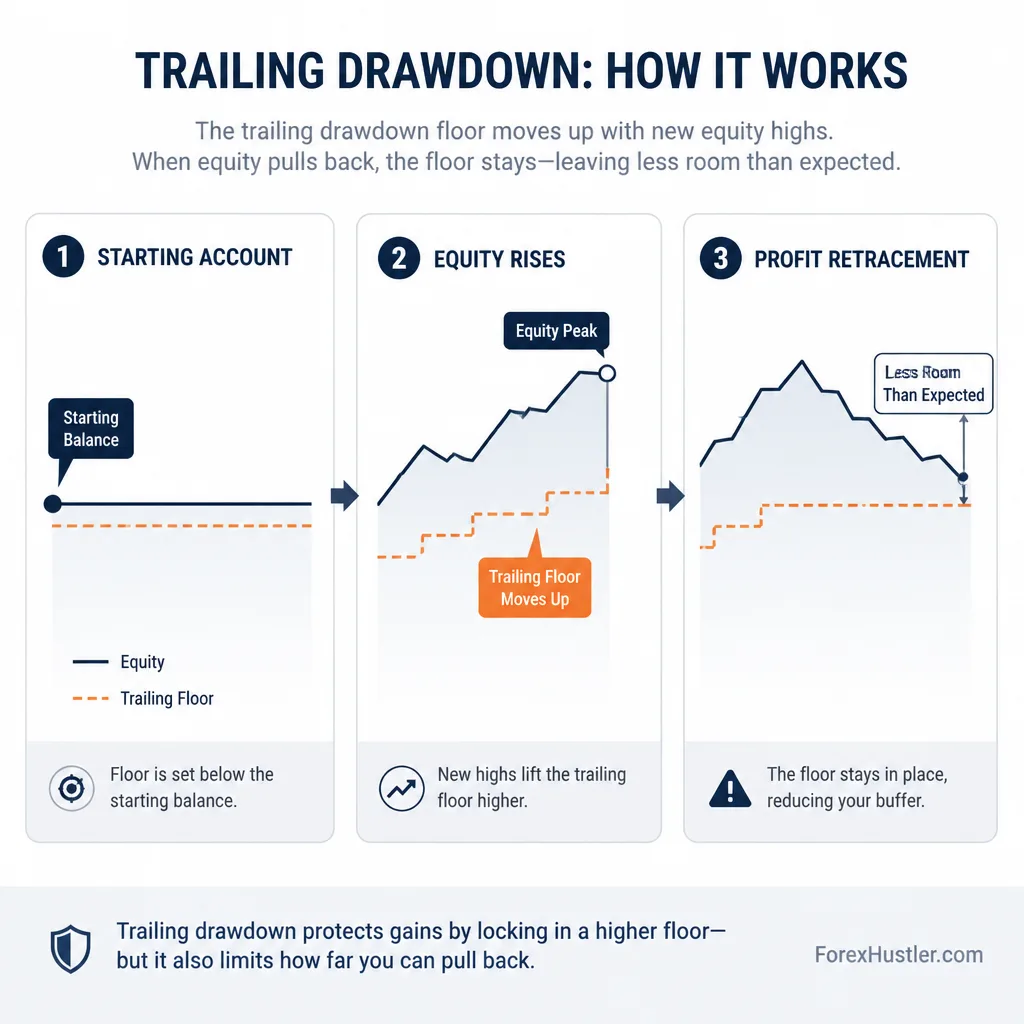

Trailing drawdown: why open profit can quietly raise the floor under your account

Trailing drawdown is the rule traders misunderstand most.

In plain English, it is a moving loss floor that follows your account higher as your balance or equity rises. But the mechanics vary a lot. Some firms trail intraday. Some trail at end of day. Some use balance. Others use equity. In some models, unrealized gains matter. In others, only closed results do.[^3]

That is not technical trivia. It changes trade management.

A simple example: you catch a strong move and your account equity rises sharply. You feel safer because you are in profit. But if your drawdown floor has ratcheted upward with that profit, the account may actually have less future flexibility than you think. If you then allow too much retracement, you can close the trade green and still end up in a tighter operating position.

That is the hidden problem with trailing drawdown. Balance safety and compliance safety stop being the same thing.

News restrictions and consistency rules: where timing matters as much as direction

Many firms restrict trading around high-impact news. The details vary. Some prohibit opening or closing trades in a blackout window. Some restrict holding exposure through the event. Some define restricted events explicitly in their rule pages or calendars.[^4]

If your edge depends on macro releases, CPI spikes, NFP volatility, or fast post-news breakouts, this is not a small inconvenience. It may remove the exact conditions your strategy needs.

Consistency rules create a different kind of pressure. They are not standardized, but they often discourage one oversized day from carrying the entire evaluation or erratic changes in risk behavior.[^5]

The practical takeaway is blunt: timing rules can invalidate a strategy even when your directional bias is right.

Why Common “Fast Money” Tactics Usually Collide With Prop Rules

Some tactics look attractive because they produce smooth short-term results. The problem is that prop rules care a lot about tail risk.

Martingale and grid systems: small wins, catastrophic rule breaches

Martingale systems increase size after losses. Grid systems layer positions as price moves. Both can produce long stretches of small wins.

That is also why they break in prop environments.

A hard daily loss cap does not care that your recovery logic usually works eventually. If the adverse move expands before the sequence can recover, the rulebook ends the account first. The strategy never gets the time it needs to prove itself.

The flaw is structural. Martingale requires room to escalate risk. Prop firms are built to remove that room.

Averaging down and adding exposure: how one idea becomes correlated account risk

Averaging down feels controlled when each entry is small.

But multiple entries are not multiple ideas if they all lose for the same reason.

A trader long EUR/USD, GBP/USD, and gold during a dollar-driven macro move may think each position is modest. In reality, those trades can behave like one oversized USD bet. When the catalyst hits, all three positions can move against the account at once.

That is why prop risk has to be measured at the account level, not one ticket at a time.

Holding winners too loosely under trailing drawdown

In a personal account, giving a strong winner room to breathe can be sensible. Under some trailing drawdown models, it becomes awkward.

If open equity lifts the drawdown floor, a large floating gain is not just potential profit. It can also tighten the compliance structure around the account. Let too much of it evaporate, and the next trade starts from a worse place than expected.

This does not mean you must scalp everything. It means your management style has to fit the drawdown model.

Overtrading low-quality setups to make the day back

This is one of the oldest prop failure patterns.

A trader starts with two ordinary losses. Nothing unusual. But now the day feels damaged. Instead of accepting the red session, they take weaker setups, lower their standards, or increase size slightly because the next trade should recover the loss.

That is exactly what max daily loss is designed to punish.

The rule is external. The emotional trigger is internal. Together, they are lethal.

How to Engineer a Rule-Aware Version of Your Existing Strategy

The goal is not to invent a new system from scratch. It is to reshape your current edge so it can survive the rule set.

Start with the account limits, not the entry signal

Work backward from the rulebook.

At minimum, define:

- daily loss limit

- total drawdown limit

- whether drawdown is static or trailing

- whether trailing is balance-based, equity-based, intraday, or end-of-day

- news restrictions

- overnight or weekend holding rules

- any consistency or payout constraints

Then convert each rule into an operating guardrail.

That order matters. If you start with entries and bolt on rules later, you usually end up with a strategy that is mathematically fine but operationally unstable.

Choose risk per trade that fits the daily loss cap

There is no universal safe percentage. It depends on your loss clustering, stop size, win rate, and the firm’s specific rules.

Still, many prop traders are better served by small fractional risk than by aggressive 1% models. If the daily cap is tight, risking too much per trade means ordinary variance can end the session before the strategy has enough attempts to express its edge.

A practical way to think about it: your per-trade risk should leave room for a normal bad day, not just one ideal setup.

Build a daily stop rule before the market opens

Your internal stop should sit inside the firm’s hard limit.

For example, if the firm’s daily breach level is tight, you might decide that after a certain loss threshold, the day is over regardless of what the rulebook technically still allows. That buffer is there for slippage, execution mistakes, and deteriorating judgment.

The firm’s limit is an emergency wall. Your limit should be the line you stop at first.

Add a “no new trades after X% drawdown” guardrail

This is one of the most useful rules you can build.

It is not exactly the same as a daily stop. It is a slowdown threshold.

After losing a predetermined share of your daily risk budget, you might allow only one A+ setup, or no new trades at all. The point is to stop trading from becoming more impulsive as your available room shrinks.

That rule protects you from the most dangerous sentence in prop trading: I still have a little room left.

Cap total open exposure, not just single-trade risk

Single-trade risk can look tidy while account-level exposure becomes reckless.

Cap:

- maximum number of open positions

- maximum total open risk

- maximum correlated exposure by theme or currency

- whether adding to a winner is allowed, and under what conditions

If three trades all depend on the same macro move, treat them as one idea for risk purposes.

Restrict trading to sessions where your edge is strongest

Session-only trading is underrated because it looks boring.

But boring is useful in prop trading.

If your tested edge appears mostly around the London session open or the New York open, trade there and stop. The rest of the day often adds churn, boredom trades, and unnecessary rule exposure.

A narrower window usually improves more than execution. It improves discipline.

Decide in advance whether your style is compatible with news restrictions

Do not treat this as something to figure out live.

If your strategy relies on scheduled volatility and the firm restricts exposure around high-impact events, you have two choices:

- redesign the strategy around non-news conditions

- admit the strategy does not fit that account

The second answer is painful, but it is better than forcing a mismatch.

A Simple Prop-Firm Risk Template You Can Adapt

This is not a universal model or personal financial advice. It is an educational template to help you turn rules into operating structure.

Suggested risk-per-trade ranges

Many traders in prop environments use conservative fractional sizing, often something like:

- 0.25% to 0.50% risk per trade for tighter rule sets

- up to around 0.75% only when the drawdown structure, loss distribution, and setup quality justify it

The point is not the exact number. The point is preserving room for variance.

If your strategy needs large per-trade risk to hit the target quickly, it may not be prop-friendly.

Daily stop logic and reset conditions

A practical template might look like this:

- define a hard personal daily stop before the firm’s limit

- stop trading after 2 to 3 full losses, depending on your model

- no restarting the session later out of frustration

- next-day reset only after journaling the losses and confirming no rule drift occurred

Many breaches happen on the trade after the plan was already broken.

Example guardrails for trade count and exposure

You might set rules like:

- maximum 2 to 4 trades per session

- maximum 1 to 2 active ideas at once

- no more than a set share of account risk tied to one currency theme, index theme, or news catalyst

- no adding to losers

- scaling into winners only if total exposure stays inside the cap

These rules are simple, but they do something important: they turn discipline into structure.

When to stand down for the day

Stand down when:

- your remaining drawdown room is too small for clean execution

- major news creates rule ambiguity

- market conditions are outside your tested playbook

- you feel the urge to recover rather than execute

- you are taking setups because the clock is running, not because the edge is present

Sometimes the best prop decision is to protect the account by doing nothing.

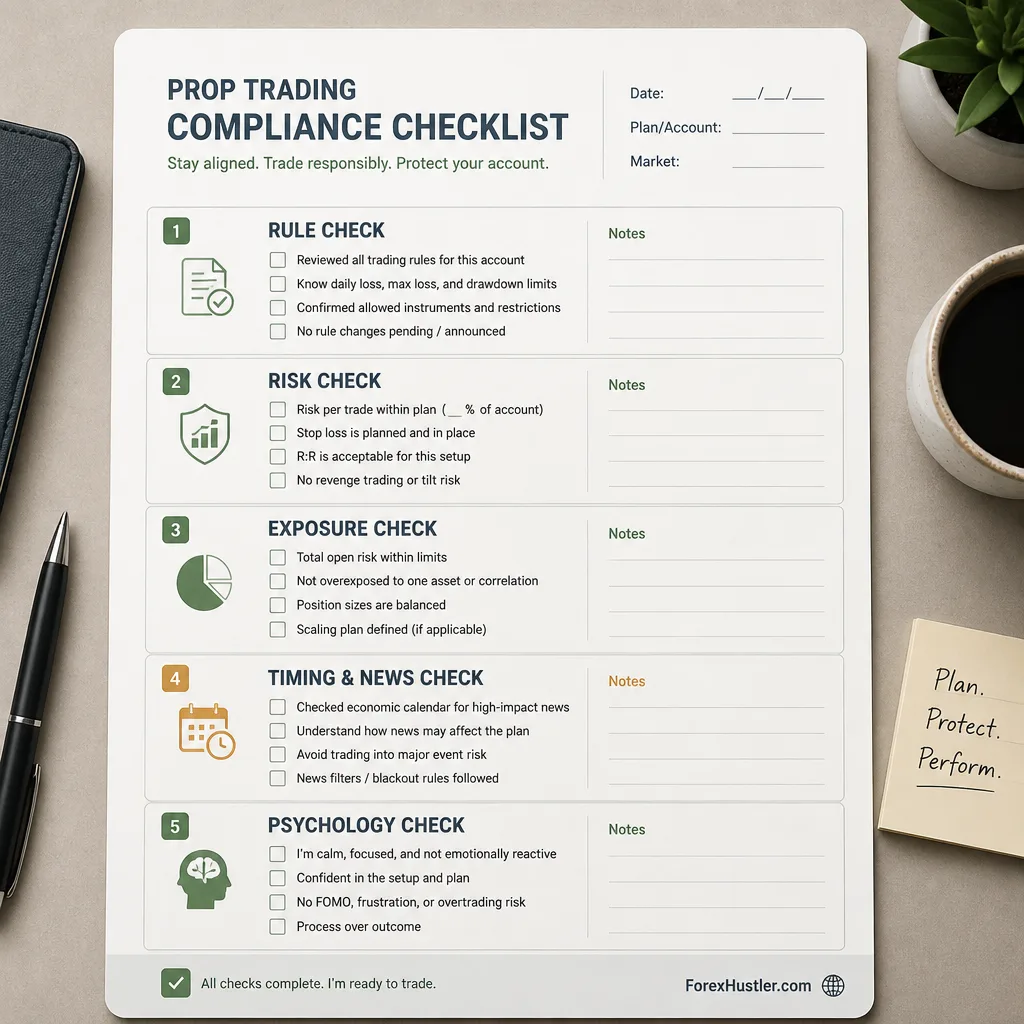

Pre-Trade Compliance Checklist

A setup is not valid unless it clears both market logic and rule logic.

Rule check

- Does this trade comply with the firm’s current rulebook?

- Am I inside any news blackout window?

- Is overnight or weekend holding relevant here?

- Are there any instrument-specific or size-related restrictions?

Risk check

- What is the exact cash and percentage risk on this trade?

- How much daily loss room remains?

- If this trade loses, do I still remain inside my personal stop structure?

Exposure check

- How many positions are already open?

- Are those trades correlated?

- Am I stacking the same idea in different symbols?

Timing and news check

- Is this within my approved session window?

- Is high-impact news close enough to distort the setup or violate rules?

- Is this trade being taken in the environment where the strategy was actually tested?

Psychology check

- Am I calm, or am I trying to repair the day?

- Did I just take losses that are pushing me toward revenge trading?

- Would I take this exact setup at the same size if I were green on the day?

If the last answer is no, the trade is usually invalid.

Failure Cases Traders Usually Miss

A lot of sensible-looking tactics fail in prop trading for reasons that are not obvious until later.

When trailing drawdown makes swing-style management awkward

Swing trading is not automatically incompatible with prop firms. But under tighter trailing models, especially where equity matters, large floating profit swings can create compliance pressure that makes wider management uncomfortable.

The issue is not whether the market eventually goes your way. It is whether the path is survivable under the rule structure.

When a high win-rate system is still too volatile

A system that wins often can still be a poor fit if its losses cluster hard or if the occasional bad sequence is large relative to the daily cap.

This is common with strategies that look stable in backtests because they smooth risk through scaling, averaging down, or delayed stops. In a prop account, the tail matters more than the smooth middle.

When partial profits help psychologically but hurt consistency

Partials can make execution easier. They can also quietly damage expectancy if the remaining position is too small to pay for your full-loss events.

That matters even more in prop trading because challenge fees, minimum days, payout pacing, and rule pressure often reward steadier expectancy, not just emotional comfort.

When the right move is to slow down, not optimize harder

Some traders keep tweaking entries because they think the problem is precision.

Often it is not.

If your method keeps colliding with daily loss, news windows, or exposure spikes, the answer may be lower frequency, smaller risk, fewer sessions, and stricter stand-down rules. That feels less ambitious. It is usually more professional.

The Real Goal Is Not Passing Fast. It Is Staying Funded Long Enough to Get Paid

The traders who survive prop firms tend to make a quiet shift in thinking. They stop asking how to hit the target quickly and start asking how to remain tradable under the rules.

That shift changes everything.

It leads to smaller risk, fewer forced trades, tighter exposure control, cleaner session selection, and a willingness to stand down when conditions do not fit. It also leads to a more honest conclusion when a strategy simply does not belong in a particular firm’s structure.

A prop strategy is not just an entry model. It is an operating model built around constraints. The sooner you treat max daily loss, trailing drawdown, and timing restrictions as design inputs rather than afterthoughts, the better your chances of doing what actually matters: staying funded long enough for your edge to get paid.

FAQ

What is max daily loss in a prop firm?

Max daily loss is the largest loss you are allowed to take in a single trading day before violating the firm’s rules. The exact calculation varies by firm. Some use start-of-day balance, others use previous end-of-day balance, and some factor in current equity. In practice, it acts as a hard intraday circuit breaker, so your strategy needs an internal stop before that hard limit is reached.

How does trailing drawdown work in prop trading?

Trailing drawdown is a moving loss limit that follows your account balance or equity as it rises. The details matter. Some firms trail intraday, some at end of day, some use balance, and others use equity. That changes how much room you really have. A trader can make money on a trade and still tighten the drawdown floor enough to make future trades harder to manage.

Why do traders fail prop firm challenges even with a decent strategy?

Many traders do not fail because they cannot find entries. They fail because their personal-account strategy was never designed for rule-heavy conditions. Max daily loss punishes recovery trading, trailing drawdown changes how winners can be managed, and news restrictions can remove the exact volatility windows a strategy depends on.

Is 1% risk per trade too much for a prop firm challenge?

Sometimes, yes. It depends on the firm’s daily loss cap, total drawdown structure, your win rate, and how often losses cluster. Under a tight daily loss limit, two normal losses plus spread or slippage can consume most of the day’s room. That is why many traders use smaller fractional risk in prop environments. Any percentage should be treated as an educational example, not a universal rule.

Why are martingale and grid strategies risky for prop firms?

They tend to hide tail risk until one expansion move breaks the account. Martingale increases size into adverse movement, which directly collides with hard daily and overall drawdown limits. Grid systems can look smooth in quiet markets but often behave like one oversized directional bet in trends. Prop rules usually end the account before the recovery logic has time to work.

How should I build a prop-firm-safe risk model?

Start with the rulebook, not the setup. Define the firm’s daily loss, total drawdown, drawdown type, news restrictions, and any consistency rules. Then convert those into guardrails: smaller risk per trade, a daily kill switch, a no-new-trades threshold after drawdown, a cap on correlated exposure, session-only trading, and a pre-trade compliance checklist.

Do news restrictions really change strategy design?

Yes, sometimes dramatically. If your edge depends on macro releases or sharp breakout volatility, a blackout window around high-impact news can remove your best setups. That makes news rules a strategy issue, not just a compliance detail. In some cases, the right conclusion is not to tweak execution but to admit the strategy does not fit that firm’s conditions.

What is the difference between static and trailing drawdown?

Static drawdown stays fixed, which makes planning simpler because the loss floor does not move. Trailing drawdown rises as your account rises, which can reduce flexibility and force tighter management of open profit and future risk. For many traders, trailing drawdown is harder because balance safety and compliance safety stop being the same thing.

Why should prop traders use a daily stop before the firm’s limit?

Because waiting to stop at the firm’s hard limit usually means you are already trading poorly, emotionally compromised, or out of room to make good decisions. An internal stop creates a buffer for slippage, execution error, and tilt. It turns the firm’s external rule into your own operating rule, which is far more useful in real time.

What is a good pre-trade compliance checklist for prop trading?

A solid checklist should cover five things: rule status, current drawdown room, planned trade risk, total correlated exposure across open positions, and timing restrictions such as session validity or nearby news. It should also include a psychology check, because many rule breaches happen after a trader is already trying to recover, force trades, or speed up the challenge.