Can You Make a Living Trading Online? A Reality-Check Framework for Income, Risk, and Time

If you’re asking whether you can make a living trading online, you probably don’t want motivation. You want to know whether trading can realistically replace your job income without creating constant financial stress.

For some traders, the answer is yes. But it is far harder than most people think. The real question is not whether trading income exists. It is whether your capital, results, and risk tolerance can support real life after taxes, costs, and losing months.

This article gives you a practical way to test that. We’ll use a simple framework built around living expenses, taxes, trading costs, drawdown tolerance, expectancy, and account size. By the end, you should be able to place yourself honestly in one of three categories: viable now, close but not ready, or not yet.

Can You Make a Living Trading Online?

The short answer: possible, but difficult

Yes, some people do make a living trading online. But most traders underestimate three things: how much capital they need, how consistent they must be, and how damaging financial pressure can become.

You can be profitable and still be nowhere near ready to trade full-time. That distinction matters. Profitability is not the same as lifestyle viability.

A better way to think about trading is as a variable-income business. Your account is the productive asset. If you need to withdraw too much from it, the whole setup becomes fragile.

Why “how much can traders make?” is the wrong question

“How much can traders make?” sounds useful, but it points you in the wrong direction. It focuses on what is possible for someone, somewhere, instead of what is realistic for you.

A trader may make 50% or even 100% in a strong year. That does not tell you whether your own account can safely produce enough spendable income to cover rent, groceries, insurance, taxes, and weak periods.

The better question is: what return would I need from my account to live on trading? Once you calculate that, the fantasy usually gives way to a clearer decision.

The real test

The real test is simple: can your trading support your life after costs, taxes, and bad months?

If your plan only works in strong months, it is not a plan. If it ignores taxes, commissions, slippage, platform fees, or data costs, it is incomplete. If it assumes you can withdraw nearly everything you make, it leaves no room for drawdowns.

Before asking whether full-time trading is possible in general, ask whether your numbers make it possible in practice.

What “Making a Living” Actually Means

Salary replacement is not the same as trading profits

A salary is usually stable. Trading income is not.

With a paycheck, you can budget around regular cash flow. With trading, you may have a strong month, a flat month, and a losing month back to back. That means your trading income has to do more than match your salary once. It has to survive variability.

If you need $4,500 a month to live, trading is not viable just because you made $5,000 last month. You need a process that can support that requirement over time, including rough periods.

Net income matters more than gross returns

Gross returns are not spendable income.

A trader might say, “I made $6,000 this month.” But what remains after commissions, slippage, platform fees, data costs, and taxes? And how much should stay in the account to preserve position sizing and absorb future losses?

That $6,000 can shrink quickly. Once you account for costs, taxes, and the need to keep some profits in the account, the amount available for living expenses may be much lower than it first appears.

That is why net income matters far more than headline returns.

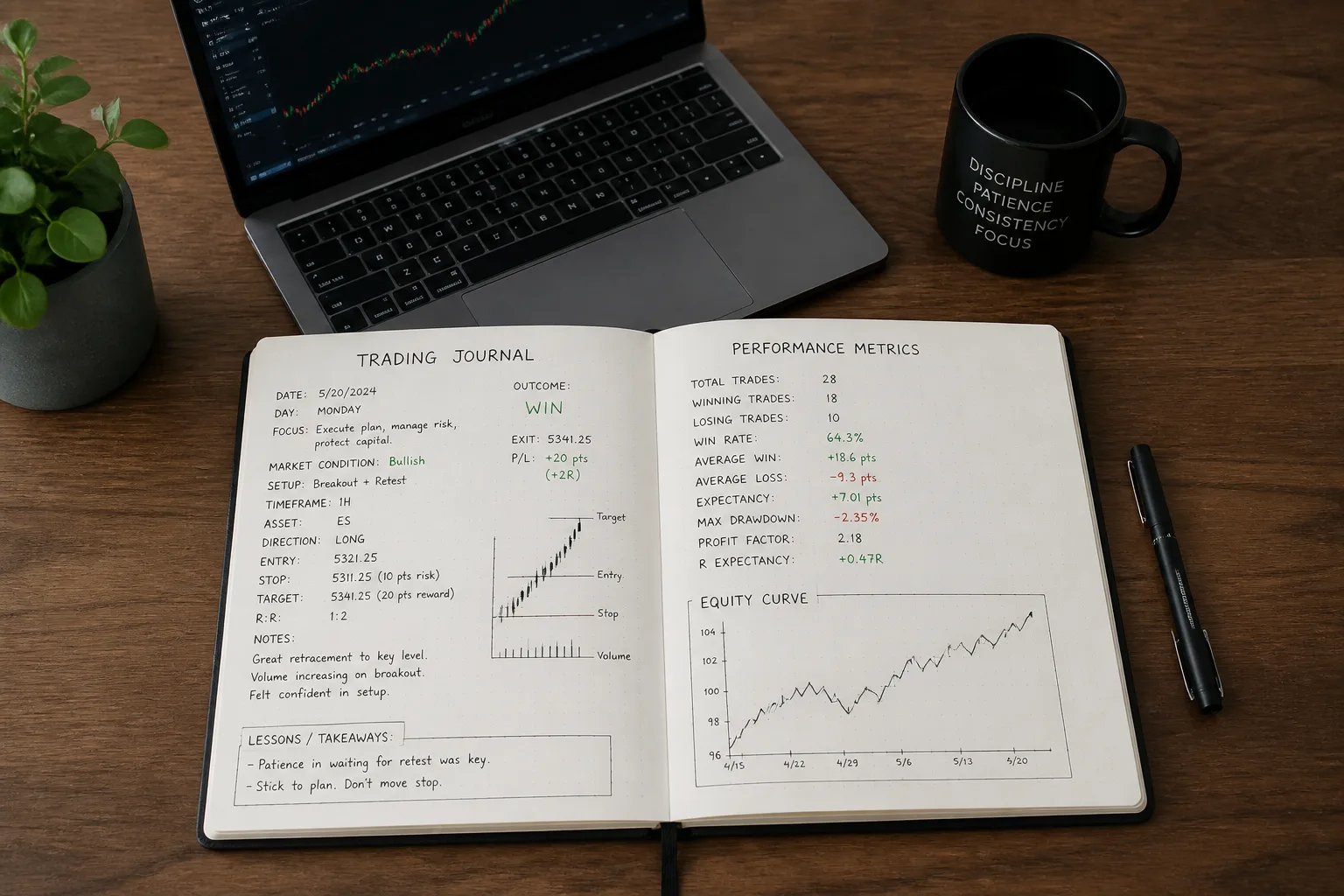

Why consistency matters more than one strong month

One or two good months do not prove much.

A better rule is to review at least 12 months of live results, and ideally 12 to 24 months. That gives you a more reliable picture of how your strategy behaves across different market conditions.

You are not just looking for profit. You are looking for:

- how many losing months you had

- your maximum drawdown

- whether results were concentrated in one unusual stretch

- whether your execution stayed disciplined under pressure

Consistency is what turns a trading method into a possible income source.

The Trading-for-a-Living Viability Framework

Use this simple model: the Living Income Trading Viability Framework.

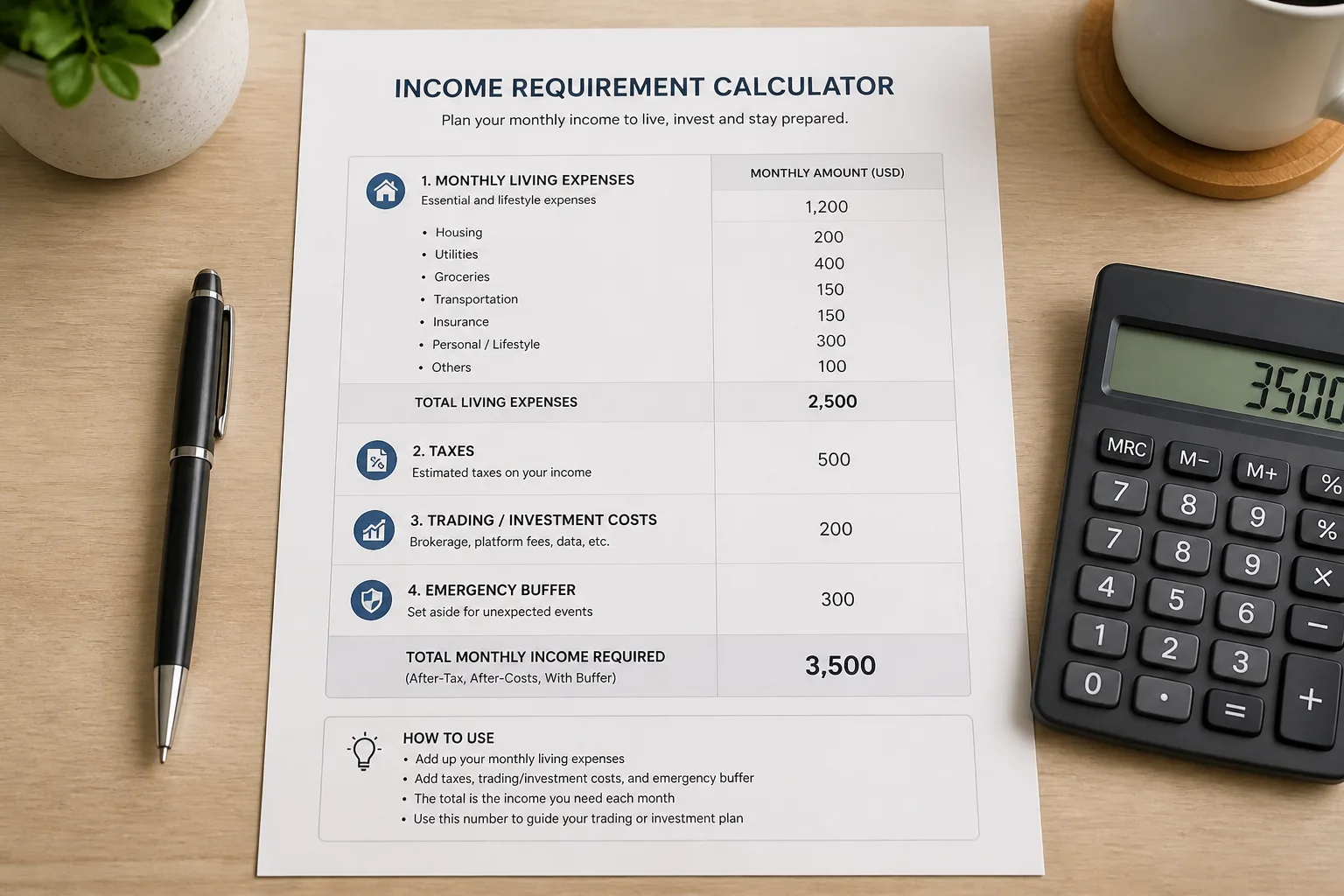

Step 1: Calculate your real monthly living number

Start with what your household actually needs each month.

Include:

- housing

- food

- utilities

- insurance

- healthcare

- transport

- debt payments

- family support

- baseline discretionary spending

Then add a modest safety margin.

Do not use an idealized “lean” budget unless that is already how you live. Use your real number. If your true monthly need is $4,500, that is the number your trading plan has to support.

Step 2: Add taxes, trading costs, and a buffer

Trading income is not fully yours to spend.

Tax treatment varies by country, instrument, holding period, and legal structure, so verify the details with a qualified tax professional. For planning, use a conservative estimate instead of assuming taxes will somehow work themselves out.

Also include recurring trading costs such as:

- commissions

- slippage

- platform fees

- data subscriptions

- internet or software directly tied to trading

Then add a buffer. Real life includes irregular expenses and weak months. A plan with no buffer is brittle.

Step 3: Define your maximum acceptable drawdown

Drawdown is not just a statistic. It is the decline in account equity you have to survive both financially and emotionally.

Recovery is asymmetric. A 20% drawdown requires a 25% gain to recover. A 50% drawdown requires a 100% gain.

If your plan requires regular withdrawals while the account is under drawdown pressure, the math gets difficult fast. A viable full-time setup has to survive ordinary losing streaks without forcing you to increase risk or pull money out at the worst time.

Step 4: Estimate realistic expectancy, not best-case returns

Expectancy is your average outcome per trade after wins, losses, and costs.

In simple terms:

Expectancy = (win rate × average win) - (loss rate × average loss) - average trading cost

That helps you judge whether your edge is real. But positive expectancy alone is not enough. You also need enough sample size, enough consistency, and enough capital.

Use live results if possible, then apply a conservative haircut. If your trailing 12-month net return is 22%, do not build a life plan around 35% because one strong quarter felt exceptional.

Step 5: Compare your income needs with your capital and results

This is the key step.

Once you know what your life requires, compare that with:

- your account size

- your live net performance

- your drawdown history

- your losing months

- your withdrawal needs

If the required return is far above what you have actually demonstrated, you are not ready yet. If the withdrawals leave no room for weak periods, the setup is fragile even if it looks fine on paper.

A Simple Formula to Stress-Test Your Plan

From monthly spending to required annual trading income

Use this formula:

Required annual pre-tax trading income = (monthly net living need × 12 + annual trading costs) ÷ (1 - estimated tax rate)

This converts your monthly household need into the gross profit your trading has to produce before taxes.

From income target to required account performance

Then calculate:

Required annual return = required annual pre-tax trading income ÷ trading capital

This tells you what your account must earn each year just to support your lifestyle.

You can also use a basic withdrawal pressure check:

Monthly withdrawal rate = monthly living need ÷ account balance

The higher this number, the more pressure you place on the account.

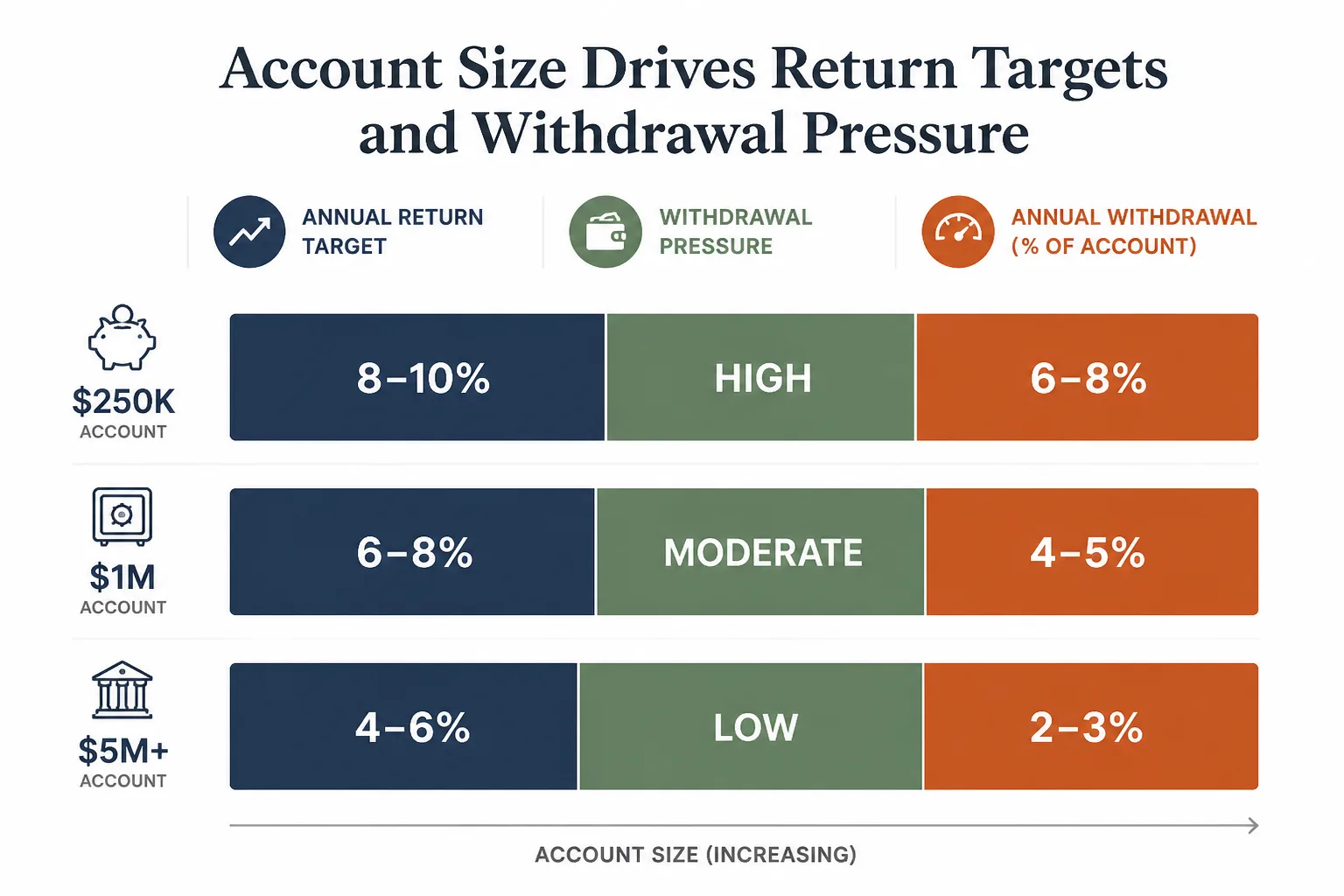

Why high required returns usually mean undercapitalization

This is one of the clearest reality checks in trading.

If your plan requires triple-digit annual returns just to pay bills, the problem is usually not motivation. It is undercapitalization.

Could someone produce those returns for a period? Maybe. Can most retail traders rely on that as a stable income plan? That is a much harder claim.

High required returns usually mean:

- too little capital

- too much withdrawal pressure

- too little room for drawdowns

- too much temptation to over-leverage

In plain English, the account is being asked to do too much.

Worked Example: Could This Trader Realistically Go Full-Time?

Example inputs

Assume a trader has:

- monthly living need: $4,500

- annual trading costs: $2,000

- estimated effective tax rate: 25%

- trading capital: $50,000

- trailing 12-month net return: 22%

- maximum drawdown: 14%

On the surface, this trader looks solid. They are profitable and reasonably disciplined. But can they trade for a living?

Applying the framework

First, annual net living need:

$4,500 × 12 = $54,000

Add annual trading costs:

$54,000 + $2,000 = $56,000

Adjust for taxes:

$56,000 ÷ 0.75 = about $74,667 required pre-tax trading income

Now compare that with capital:

$74,667 ÷ $50,000 = about 149% required annual return

That is the stress test.

This trader’s actual trailing return is 22% net. The plan requires about 149% before tax just to support basic living expenses. That gap is not small. It is a clear warning sign.

What the example shows

This trader is not yet ready to go full-time.

The issue is not a total lack of skill. It is a mismatch between capital and income needs. The account is too small relative to the required withdrawals.

Now compare that with a trader holding $200,000 in capital with the same living costs and similar tax assumptions. The required pre-tax income is still about $74,667, but the required annual return drops to about 37.3%.

That is still demanding, but it is far more plausible than 149%, especially if the trader has a multi-year record, controlled drawdowns, and separate cash reserves.

Where Traders Misjudge the Math

Using peak months instead of long-term averages

Your best month is not your business model.

Many traders anchor on their hottest stretch. But a living-income plan should be based on average or median net performance over a meaningful sample, not on a period when market conditions happened to suit your strategy perfectly.

Ignoring losing streaks and drawdowns

A plan that assumes every month will be positive is fantasy.

Even profitable traders have losing months. Sequence-of-returns risk matters here. If a bad stretch happens early while you are making withdrawals, the account can come under pressure much faster than your annual average suggests.

Assuming all profits are available to withdraw

Not every dollar of profit should leave the account.

Some of it needs to stay in place to maintain position sizing, absorb variance, and keep the account from shrinking into a weaker base. This is one reason smaller accounts struggle to support household income even when they are profitable.

Underestimating the pressure of paying bills from trading

This part is often ignored until it becomes a problem.

When rent depends on this week’s trades, execution changes. Traders force entries, overtrade, widen risk, or break rules because the trade is no longer just a trade. It becomes a bill-payment event.

That pressure can damage a strategy that worked well when the stakes felt lower.

Time, Skill, and Psychological Load Matter Too

More screen time does not guarantee more income

Many beginners assume that full-time trading means more hours and therefore more money.

Usually, it does not work that way. More screen time often leads to more low-quality trades. For many strategies, edge comes from selectivity, not constant activity.

The question is not “How many hours can I watch charts?” It is “Can I execute a real edge repeatedly?”

A strategy is not the same as a repeatable process

A strategy is an idea. A process is an operating system.

A repeatable process includes:

- market selection

- entry criteria

- position sizing

- risk limits

- journaling

- review routines

- rules for standing aside

This matters because full-time trading exposes every weakness in execution. If your results depend on intuition, mood, or favorable conditions, they may not hold up when trading becomes your primary income source.

Why financial pressure damages execution

Pressure narrows thinking.

A trader under income stress may take setups that are not there, increase size after losses, or trade simply because they feel they need to make money today. That breaks the link between edge and execution.

So even if the numbers look close, ask whether your psychology is strong enough for the transition.

Decision Framework: Are You Ready, Close, or Not Yet?

Signs you may be closer than you think

You may be closer if you have:

- 12 to 24 months of tracked live results

- profitability across different conditions

- withdrawal needs that imply realistic returns

- manageable drawdowns

- a separate emergency fund

- clear risk rules and process discipline

In that case, a cautious transition may make sense.

Signs you should stay part-time for now

You should probably stay part-time if you have:

- a short or inconsistent track record

- profits concentrated in one unusually strong period

- a required annual return above your demonstrated results

- no cash reserve outside the trading account

- dependence on high leverage

- repeated rule-breaking under pressure

This does not mean you should quit trading. It means you should not rely on it yet.

A practical middle path

The middle path is often better than a clean leap.

You could:

- keep your job while extending your live track record

- build more capital before relying on withdrawals

- reduce work hours gradually if possible

- create 6 to 12 months of cash reserves

- test a staged withdrawal plan before quitting

That approach reduces pressure and gives your numbers more time to prove themselves.

Final Reality Check

Trading for a living is a numbers problem before it becomes a lifestyle decision.

Yes, it is possible to make a living trading online. But that only matters if your current setup can produce sustainable net withdrawals without requiring extreme returns, excessive leverage, or constant emotional strain.

Run the framework on your own results. Use at least 12 months of live data, and preferably 24. Be conservative with taxes, honest about costs, and realistic about drawdowns. If the numbers support a cautious transition, you may be close. If they do not, the smarter move is usually to keep building skill, capital, and stability first.

FAQ

Can you make a living trading online?

Yes, some traders do. But the harder question is whether your own numbers support it. A viable plan depends on enough capital, consistent live results, manageable drawdowns, realistic withdrawals, and a clear view of taxes and costs.

What does making a living from trading actually mean?

It means generating sustainable net withdrawals that cover real living expenses without forcing reckless risk-taking. It is not the same as having a few profitable months or attractive returns on paper.

How much money do you need to trade for a living?

There is no universal number. It depends on your monthly expenses, taxes, trading costs, drawdown tolerance, and actual performance. The key test is whether the required annual return on your account is realistic based on your live track record.

Why is salary replacement different from trading profits?

A salary is usually smoother and easier to budget around. Trading income is variable and uncertain. Trading profits also have to absorb taxes, commissions, slippage, platform costs, and losing periods before they become spendable income.

How do you calculate whether full-time trading is financially viable?

Start with your real monthly living need, add annual trading costs, adjust for taxes, and compare the required pre-tax income with your trading capital and historical net performance. If the implied return is far above your demonstrated results, the plan is probably not viable yet.

What is a realistic way to estimate trading expectancy?

Keep it simple: expectancy is your average outcome per trade after wins, losses, and costs. Use live data from a meaningful sample and apply a conservative haircut rather than assuming your best recent period will continue.

Why do high required returns usually signal undercapitalization?

If your account needs extreme annual returns just to pay your bills, you are probably trying to draw too much income from too little capital. That increases pressure, encourages excess risk, and leaves little room for normal drawdowns or weak periods.

How many months of results should you review before considering full-time trading?

At a minimum, review 12 months of live, tracked results. Ideally, use 12 to 24 months so you can see how your strategy behaves across different conditions, including losing months and drawdowns.

Can a profitable trader still be unready to trade full-time?

Yes. A trader can be profitable but still lack enough capital, consistency, cash reserves, or emotional stability to depend on trading for household income. Profitability alone does not guarantee lifestyle viability.

Should you quit your job as soon as trading becomes profitable?

Usually not. A staged transition is often better: extend your live track record, build more capital, maintain an emergency fund, and test whether your results can support withdrawals without damaging execution.