Portfolio Rebalancing for Long-Term Investors: When to Rebalance, How Much, and What It Actually Fixes

Many investors assume portfolio rebalancing exists to boost returns. The idea is appealing: sell what has gone up, buy what has lagged, and collect a neat “sell high, buy low” benefit.

That can happen. But it is not the main point.

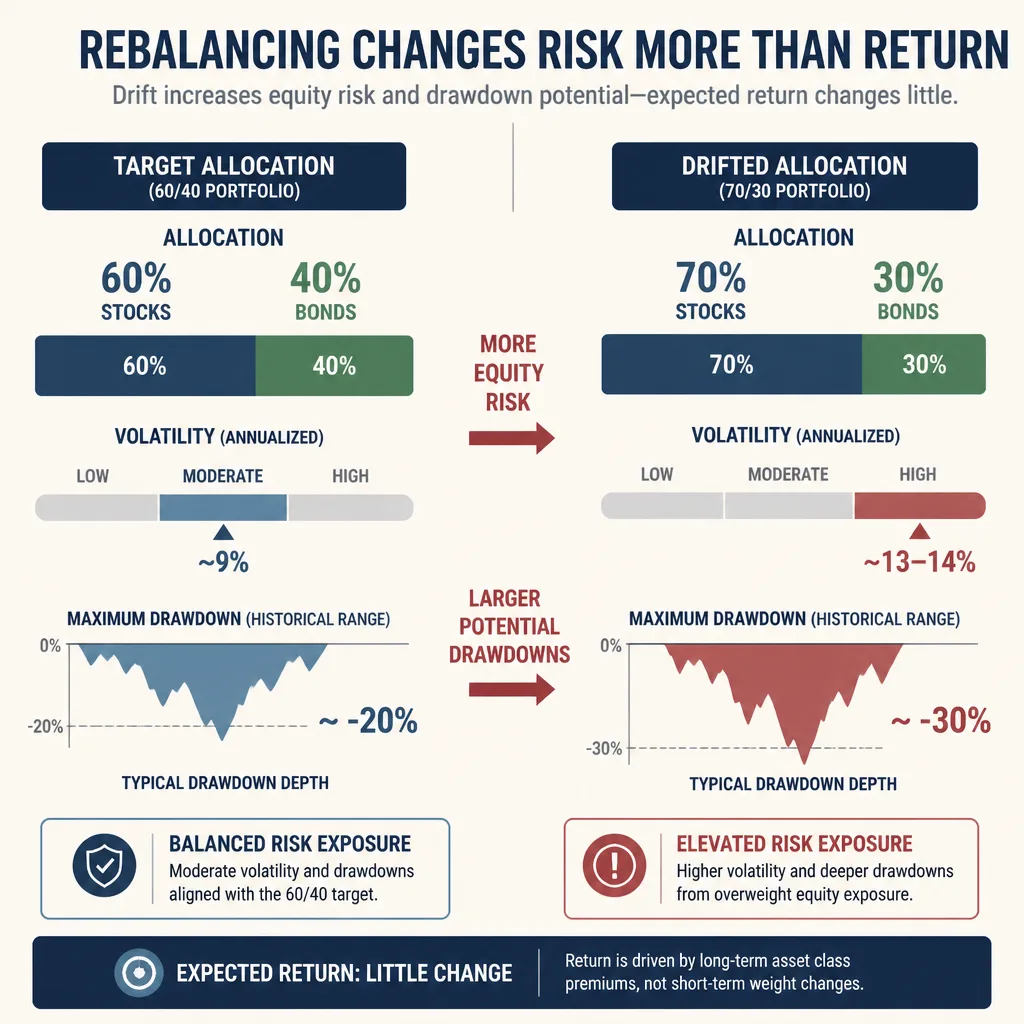

For long-term investors, rebalancing is mostly a risk-control tool. Its job is to keep a portfolio from quietly turning into something you never meant to own. A 60/40 portfolio does not stay 60/40 by itself. After a strong run in stocks, it can drift to 70/30 or beyond, bringing more equity risk, deeper drawdowns, and behavior that may no longer match your plan.[^1]

So the real question is not, “How do I maximize returns with rebalancing?” It is: when has drift become meaningful enough to act, and how can I correct it with the least tax, cost, and friction?

Rebalancing fixes risk drift more than return problems

What rebalancing actually changes

Rebalancing changes weights. That sounds trivial, but it matters.

If you chose a portfolio with 60% stocks and 40% bonds, that mix reflected some balance of return goals, loss tolerance, and time horizon. Rebalancing restores that choice after markets pull it off target.

The core benefit is not higher performance. It is keeping the portfolio aligned with the risk you intended to take.

A drifting portfolio is not just cosmetically different. It may now carry more volatility, larger downside exposure, and greater dependence on one asset class continuing to lead.

Why a 60/40 portfolio drifts

Imagine a $100,000 portfolio split 60/40: $60,000 in stocks and $40,000 in bonds.

Now suppose stocks rally while bonds lag. A few years later, the portfolio might look more like $84,000 in stocks and $36,000 in bonds. That is now 70/30.

Nothing broke. In fact, the investor may be pleased with the result. But the portfolio is no longer taking the same level of risk. It is now more exposed to an equity decline than intended.

That is the quiet problem rebalancing solves. Drift often builds during good times, which is why many investors overlook it.

What rebalancing can and cannot do

Rebalancing can improve discipline. It can keep risk closer to target. In some environments, especially when asset classes are volatile and not perfectly correlated, it may modestly improve risk-adjusted results.[^1][^2]

What it cannot do is reliably increase returns.

In long bull markets, especially stock-led ones, not rebalancing can outperform because the winning asset keeps growing as a larger share of the portfolio. That is a fair objection. But that outperformance usually comes from taking more risk than originally planned, not from finding a free lunch.

That distinction matters. Rebalancing is not a return engine. It is portfolio maintenance.

The first question is not how often. It is how much drift matters

A better mental model: drift is really risk change

Most investors start by asking, “How often should I rebalance?”

That is not the best starting point.

A better question is: how much drift is enough to matter?

A 2-point deviation is usually not a serious issue. A 10-point shift in a major asset class often is. Rather than aiming for constant precision, think in terms of risk. Has the portfolio become materially different from the one you meant to hold?

That framing cuts out a lot of unnecessary trading.

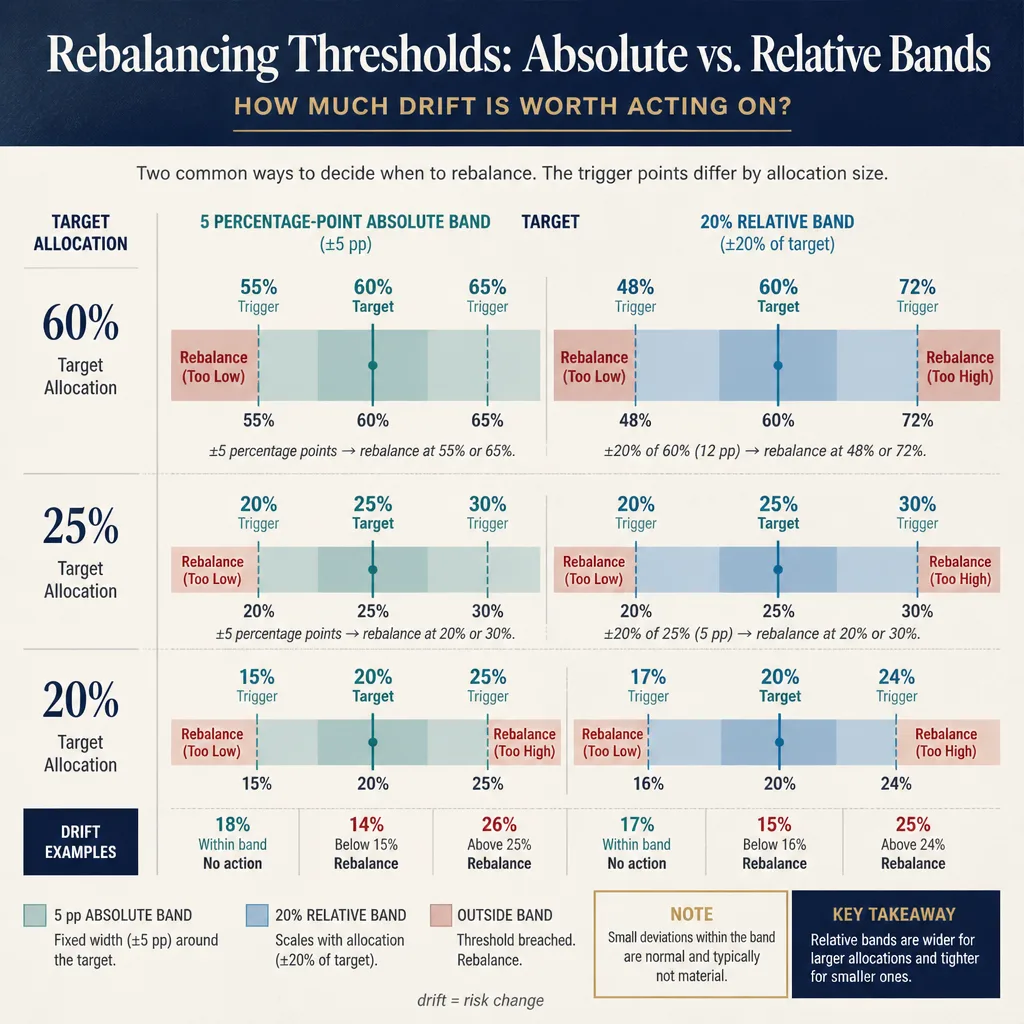

Reasonable thresholds for major asset classes

There is no universal best threshold. Research and practitioner guidance generally support tolerance bands rather than constant fine-tuning, but the right band depends on portfolio size, taxes, and trading costs.[^1][^3]

Two common rules of thumb are:

- Absolute band: rebalance when an asset class moves more than about 5 percentage points from target.

- Relative band: rebalance when an allocation drifts by about 20% of its target weight.

A few examples make the difference clearer:

- A 60% stock target under a 20% relative rule would trigger around 48% or 72%.

- A 25% international stock target would trigger around 20% or 30%.

- A 20% target drifting to 24% may not justify action under a 5-point absolute band.

These are guidelines, not laws. Big core allocations like stocks versus bonds usually matter more than small satellite positions.

Why small deviations rarely deserve action

Minor drift often looks more important on a spreadsheet than it does in practice.

If your international stock target is 20% and it drifts to 22%, the portfolio has not meaningfully changed. Selling just to restore precision may do more harm than good if it creates taxes, spreads, or unnecessary trading.

One of the most useful mindset shifts here is that good enough is often better than perfect.

Calendar vs. threshold rebalancing

Both methods can work. They just solve different problems.

Calendar rebalancing: simple and easy to follow

Calendar rebalancing means reviewing or resetting the portfolio on a schedule: annually, semiannually, or quarterly.

Its biggest advantage is behavioral. It is easy to remember, easy to automate, and less likely to turn into constant tinkering. That matters more than many investors realize. A simple process you follow is better than a more elegant one you ignore.

The weakness is that calendar rules can be both late and overactive. They may miss major drift that happens months before your review date, or they may trigger trades when the drift barely matters.

Threshold rebalancing: more responsive, often more efficient

Threshold rebalancing acts only when allocations move outside pre-set bands.

That is often more efficient because it ties action to material change, not the calendar. Research from firms like Vanguard and Charles Schwab suggests that different rebalancing methods often lead to broadly similar long-run outcomes, with the biggest differences showing up in turnover and how closely risk stays near target.[^1][^3]

The tradeoff is practical: threshold systems require monitoring. For some investors, monitoring turns into meddling.

A hybrid approach that fits most investors

For many long-term investors, the best answer is a hybrid:

- review on a light schedule, such as quarterly or semiannually

- trade only if a threshold has been breached

This gives you the structure of a calendar and the efficiency of tolerance bands.

It also helps prevent a common mistake: checking the portfolio every week and calling it discipline.

How to rebalance with less friction

A useful way to think about implementation is:

- Is the portfolio meaningfully off target?

- Can I fix the drift with cash flows instead of sales?

- Will taxes, spreads, or liquidity costs outweigh the value of precision?

That order matters.

Use contributions and distributions first

If you are still adding money regularly, new cash can do much of the work.

Suppose your U.S. stock fund has grown too large and your bond fund is underweight. Instead of selling stocks, direct the next few contributions into bonds. If you receive dividends or interest, send that cash to the underweight side as well.

For smaller or still-growing portfolios, this is often enough to narrow drift without realizing gains.

It is especially helpful in taxable accounts because it can reduce tax events while improving the allocation.

Use tax-advantaged accounts first when possible

If you hold similar exposures across retirement and taxable accounts, rebalancing inside tax-advantaged accounts often makes sense first. In many jurisdictions, trades inside retirement accounts do not create current capital gains taxes, though the details depend on the account type and country.

For U.S. investors, that often means adjusting positions in a 401(k), IRA, or Roth IRA before selling appreciated positions in a taxable brokerage account.[^4]

This is not automatic. Asset location, withdrawal plans, and account restrictions can complicate the decision. Still, as a first pass, tax-sheltered accounts are often the cleaner place to trade.

If you have to sell, pay attention to tax lots

When taxable selling is necessary, lot selection matters.

For U.S. investors, capital gains depend on cost basis and holding period, and many brokers let you choose tax lots rather than selling blindly.[^5] Selling higher-cost lots first can reduce taxable gains. Selling at a loss may also create tax benefits, subject to rules like the wash sale rule.[^5]

A realistic example: if one ETF is overweight but carries a large embedded gain, bringing it all the way back to target may be tax-inefficient. A better move might be to trim only part of it, redirect new money elsewhere, or offset gains with realized losses in another holding.

When partial rebalancing is enough

This is where many investors make the process harder than it needs to be. They assume rebalancing means returning to exact target weights.

Usually, it does not.

If your stock allocation drifts from 60% to 68%, moving it back to 63% may be perfectly reasonable if a full reset would trigger a large tax bill. The goal is to bring risk back within a sensible range, not to satisfy a spreadsheet.

Precision can be expensive. Range control is often the better tradeoff.

Where rebalancing can backfire

High tax drag in taxable accounts

This is the most common failure case.

A tidy rebalance on paper can be a poor real-world decision if it realizes substantial capital gains. In taxable accounts, implementation cost may matter more than the rebalancing rule itself.

That is why “rebalance every year no matter what” is often too blunt. Taxes are part of returns.

Illiquid holdings, wide spreads, and concentrated positions

Rebalancing gets harder when the portfolio includes more than liquid index funds.

If you own thinly traded ETFs, closed-end funds, individual small-cap stocks, private assets, or a concentrated employer stock position, trading costs and liquidity risk can be substantial. A position may be overweight, but reducing it may be expensive in both spreads and taxes.

In those cases, textbook rebalancing often turns into damage control.

Strong momentum markets

There is also a valid strategic objection: in strong momentum regimes, repeated trimming can hurt returns because you keep cutting exposure to the asset that continues to lead.

That does not mean rebalancing is wrong. It means the goal has to be clear. If the goal is strict risk control, rebalancing still makes sense. If the goal is to let trends run, wider bands and less frequent intervention may fit better.

Just do not confuse one objective with the other.

Overtrading disguised as discipline

Some investors use rebalancing as an excuse to constantly touch the portfolio.

They check allocations every week. They trim tiny deviations. They label every discretionary move as maintenance.

That is not discipline. It is overtrading with a respectable name.

A good rebalancing policy should reduce emotional decisions, not multiply them.

A simple policy many long-term investors can follow

A practical sample rule set

A workable policy for many long-term investors looks like this:

- Review the portfolio twice a year

- Rebalance only if a major asset class is off target by more than 5 percentage points or more than 20% relative to target

- Use new contributions, dividends, and interest first

- Prefer trades inside tax-advantaged accounts when possible

- If taxable sales are required, use tax-lot awareness

- Allow partial rebalancing when full precision would create high taxes or trading friction

This is not the perfect system. It is a durable one.

How often to monitor

Most investors do not need monthly checks.

Quarterly, semiannual, or annual reviews are usually enough unless the portfolio is unusually large, close to retirement, heavily concentrated, or tied to fast-moving liabilities.

The point of monitoring is to catch meaningful drift, not to stare at noise.

What to put in a written policy

A written policy is underrated because it turns rebalancing from an emotional reaction into a process.

At minimum, it should include:

- your target allocation

- what counts as meaningful drift

- how often you review

- the order in which you rebalance

- how you handle taxes and partial adjustments

Even a one-page rule set can improve decisions during market extremes, when drift is largest and emotions are loudest.

Conclusion

Portfolio rebalancing is not a magic return strategy. It is a way to stop your portfolio from drifting into a risk profile you did not choose.

That is why the key decision is not whether to rebalance monthly, annually, or with some clever formula. It is deciding how much drift actually matters, then correcting it with as little friction as possible. For most long-term investors, that means tolerance bands wide enough to avoid busywork, periodic monitoring instead of constant checking, and tax-aware implementation that uses cash flows before sales.

If you remember one thing, make it this: the best rebalancing policy is not the most precise. It is the one that keeps risk under control without creating unnecessary taxes, costs, or behavioral mistakes.

FAQ

What is portfolio rebalancing actually for?

It is mainly a risk-control process. Rebalancing brings the portfolio back toward its target allocation after market movements change the mix of assets. It is not a reliable way to maximize returns in every market.

Does rebalancing increase returns?

Not consistently. It can sometimes improve risk-adjusted outcomes, especially when asset classes are volatile and mean-reverting, but it does not guarantee higher returns. In long bull markets, not rebalancing can even outperform because the winning asset keeps compounding as a larger share of the portfolio.

How often should I rebalance?

Many long-term investors do well with a light review schedule such as quarterly, semiannually, or annually. A practical approach is to review on a schedule but trade only when allocations drift beyond pre-set thresholds.

What level of drift should trigger rebalancing?

Common rules of thumb include an absolute band of about 5 percentage points or a relative band of about 20% of the target allocation. The right threshold depends on your asset mix, taxes, trading costs, and sensitivity to risk drift.

Is calendar or threshold rebalancing better?

Neither is always better. Calendar rebalancing is simpler and easier to follow. Threshold rebalancing is more responsive and often avoids unnecessary trades. For many investors, a hybrid approach works best: review periodically and act only when drift is meaningful.

Can I rebalance without selling?

Often, yes. New contributions, redirected dividends, and interest payments can be used to buy underweight assets. This is especially useful for investors who are still adding money and want to limit taxes and turnover.

How should I rebalance in a taxable account?

Start with the lowest-friction options: direct new cash to underweight assets, consider redirecting dividends, and use tax-advantaged accounts first if you hold similar exposures there. If taxable sales are necessary, tax-lot selection and unrealized gains matter. Tax rules vary by country, so check the rules for your jurisdiction.

Should I sell winners every time they outperform?

No. Small deviations usually do not justify action. Rebalancing is about correcting meaningful drift, not trimming every gain. Selling winners too often can create unnecessary taxes, costs, and behavioral overtrading.

When does rebalancing backfire?

It can backfire when tax costs are high, holdings are illiquid, bid-ask spreads are wide, or a concentrated position has large embedded gains. It can also hurt returns in strong momentum markets if you keep trimming assets that continue moving higher.

What is a simple rebalancing policy for long-term investors?

A practical policy is to review the portfolio once or twice a year, rebalance only when major asset classes move outside a chosen band, use contributions and dividends first, prefer tax-advantaged accounts for trades, and allow partial rebalancing when taxes or trading costs are high.