Trading Forex Around CPI, NFP, and Central Bank Days: A Risk-First Playbook for Volatility Spikes

The days that look most profitable are often the days traders lose money fastest.

CPI, NFP, and central bank decisions attract attention because price can move hard. But the real challenge is not just bigger candles. The market itself changes. Spreads widen, fills get worse, and the first move can reverse before conditions stabilize.

That is why the edge on news days often has less to do with predicting direction and more to do with managing hostile conditions, waiting for price to become readable again, and knowing when not to trade. Scheduled releases from the U.S. Bureau of Labor Statistics and decisions from central banks such as the Federal Reserve, ECB, or Bank of England matter because they can shift expectations for rates, growth, and inflation.[^1][^2]

If you keep getting chopped up on major news days, the fix usually is not a better prediction model. It is a better playbook.

The real problem with CPI, NFP, and central bank days

Why these events look easy but punish retail execution

In hindsight, news trading can look simple. You see a large candle, a clean reversal, or a breakout that ran for 80 pips. What the chart does not show is the path inside that move.

A market order during a CPI release may fill several pips worse than expected. A stop placed beyond structure can get hit by spread expansion rather than genuine price acceptance. A breakout may look clean on the chart but still be difficult to enter without chasing.

That gap between visible movement and executable price is where many retail traders get hurt.

Survival is part of the edge

On major news days, capital preservation is not passive. It is part of the strategy.

The logic is simple: if market conditions are temporarily hostile to clean execution, doing less is often smarter than doing more. No trade is not a failure of nerve. It is a judgment about market quality.

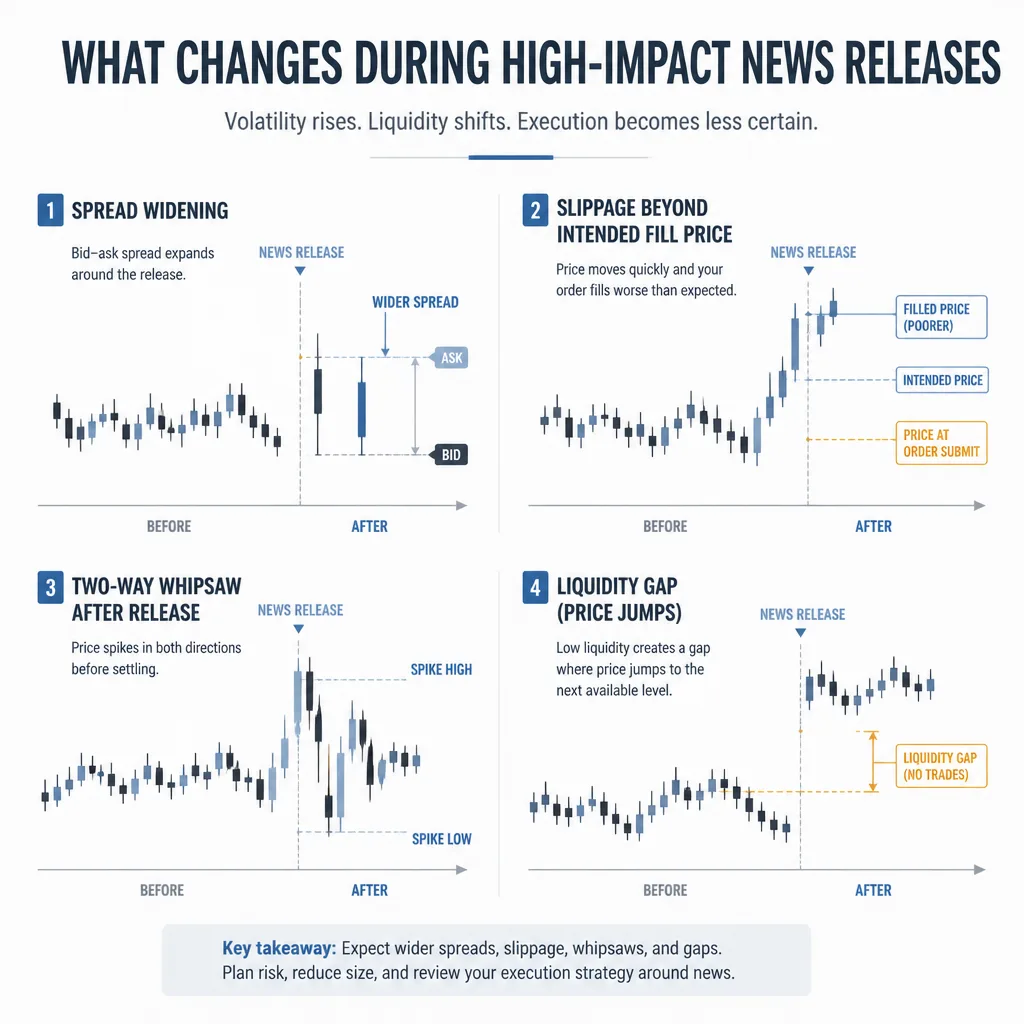

What changes when high-impact news hits

Spread widening

Around scheduled releases, liquidity providers may widen quotes before the number even drops. That increases your entry cost and makes stops easier to hit even if the trade idea has not actually failed.

A setup that works in a normal London or New York session can behave very differently during CPI or NFP.

Slippage

In fast markets, price does not always move smoothly from one level to the next. It can jump. A stop order or market order may get you in or out, but not at the price you expected.

If you planned to risk 20 pips and got filled 8 pips worse, your real risk was never 20.

Whipsaws and two-way sweeps

The first move after a release is often the least trustworthy, especially when the headline is only part of the story.

NFP is a good example. Traders focus on payrolls, but markets may also react to wages, unemployment, participation, and revisions.[^3] CPI can behave the same way when traders parse headline versus core inflation, or month-over-month versus year-over-year data.[^4]

The result can be a spike in one direction, a reversal, and then a second expansion once the details are absorbed.

Liquidity gaps

Many discretionary setups assume reasonably continuous price action. News releases break that assumption.

That matters because a lot of retail methods rely on precise entries, tight stops, and clean retests. In a thin, fast market, those tools become less reliable.

Why prediction is not enough on news days

You can be right and still lose

This is the most frustrating trap. You can correctly anticipate a hotter CPI print, weaker payrolls, or a dovish central bank tone and still lose money.

The reason is simple: analysis and execution are separate problems.

You might read the macro surprise correctly, enter too late after the first expansion, place a stop inside unstable noise, and then get slipped on the exit. The idea was right. The trade was not.

Execution risk matters as much as analysis

On event days, execution risk deserves equal weight with directional analysis.

That means asking:

- Can I get filled cleanly enough for this setup to make sense?

- Can I place a stop where the trade is actually invalidated, not where noise is likely to sweep?

- Does my broker’s execution during news make this viable at all?

These are not side questions. They are the main ones.

Retail traders are not playing the same game

Institutional participants may have better infrastructure, deeper liquidity access, and event-specific processes. Most retail traders operate through brokers whose spreads, fill policies, and platform behavior can change materially during fast markets.

The lesson is not “never trade news.” It is this: do not assume the opportunity you see on the chart is the opportunity available to you.

Three defensible ways to handle major news days

The right choice depends on your tools, experience, and broker conditions.

| Approach | Best for | Main advantage | Main limitation |

|---|---|---|---|

| Stand aside completely | Beginners, inconsistent traders, weak broker execution | Avoids the worst execution chaos | No participation in the move |

| Trade post-release structure | Most discretionary retail traders | Waits for cleaner information and better risk definition | Requires patience; may miss part of the move |

| Use options or hedged proxies where available | Traders with access and product knowledge | Can define risk differently than spot execution | Availability, complexity, and regulation vary |

1. Stand aside completely

For many developing traders, this is the right default.

If you do not have a tested event-specific method, have not studied your broker’s behavior during releases, or tend to get impulsive when volatility spikes, standing aside is not excessive caution. It is discipline.

A lot of damage happens because traders feel they should be involved in major macro days. They do not.

2. Trade the post-release structure, not the initial spike

For many retail traders, this is the most defensible active approach.

The idea is straightforward: let the release window do its violent work, then look for evidence that price is becoming tradable again. That might mean:

- a range forming after the initial burst

- a breakout that holds instead of snapping back

- a reclaim of a key level

- a pullback after directional acceptance

- a failed breakout that traps one side

For example, EUR/USD may spike lower on a hot CPI print, then spend several minutes chopping violently. Later, price retests the breakdown area, fails to reclaim it, spreads narrow, and candles stop printing oversized tails in both directions. That later retest is a very different environment from the initial spike.

3. Use options or hedged proxies where available

This is more conditional than many traders assume.

If you have access to listed FX options, currency futures options, or other regulated products, limited-risk structures can sometimes make more sense than forcing a spot trade through a chaotic release. But this depends heavily on jurisdiction, access, cost, and product knowledge.

For most spot forex traders, this is not a plug-and-play solution. Think of it as an alternative framework, not a universal recommendation.

A practical timing framework for news-day trading

The pre-release no-trade window

There is no universal rule here, and anyone claiming otherwise is oversimplifying. But many traders benefit from defining a no-trade window before the event because conditions can deteriorate before the release itself.

The key is not the exact number of minutes. The key is consistency. Pick a rule, test it, and stop improvising five minutes before the number.

What the first 1 to 5 minutes can tell you

Treat the first few minutes as an observation phase, not an obligation to act.

Watch for clues:

- Are spreads still abnormally wide?

- Are candles printing long tails in both directions?

- Is the first move being accepted or instantly faded?

- Is price holding beyond a level, or just sweeping both sides?

This is not a law. It is a practical filter.

What cleaner post-news structure looks like

A better setup usually has three traits:

Price has stopped behaving erratically.

Not calm, just less disorderly.There is a level or range that matters.

A break-and-hold, a reclaim, or a failed break you can define.The stop distance is rational relative to the target.

If the setup needs a huge stop just to survive noise, it may not be tradeable for your account.

When the market is still too messy

Walk away if:

- spreads remain unstable

- price keeps sweeping both sides

- central bank communication is still unfolding

- the press conference has become the real event

- you cannot identify a logical invalidation point

Central bank days deserve extra caution because the decision, statement, projections, and press conference can each trigger their own reaction.[^5]

Position sizing and stop placement need different rules here

Why normal size is often too large

If execution quality worsens, your normal size may quietly become too big.

That happens because chart-based risk is not the same as real risk during a release. Wider spreads and slippage mean a 15-pip stop can behave like something much larger in practice.

A simple rule helps: when volatility and execution uncertainty rise, size usually needs to fall.

Wider stops are not safer if size stays the same

A wider stop is not automatically a mistake. It becomes a mistake if you keep the same position size and increase your dollar risk.

The right sequence is:

- decide the invalidation level

- estimate realistic event-day risk, including slippage

- reduce size so total account risk still makes sense

Many traders do the opposite. They widen the stop, keep the size, and tell themselves they are being safer.

They are not.

The trap of obvious pre-news highs and lows

Pre-news highs, lows, and tight intraday ranges often look like logical structure. On normal days, they may be.

On major releases, they are also obvious sweep points.

That does not mean those levels never work. It means their reliability changes when price discovery becomes discontinuous. A stop tucked just beyond a pre-news high or low can be technically logical and still fragile in practice.

Sometimes the best stop is no trade

If the only honest stop location is too wide for your account, or if likely slippage makes your planned risk unacceptable, the setup is not structurally tradeable.

At that point, no trade is the best stop you can place.

How to backtest news-day filters without fooling yourself

Separate event days from normal days

Do not blend CPI, NFP, and central bank days into your normal sample and assume you have a clean edge.

These are different environments. Test them separately.

Do not assume perfect fills

This is where many news backtests turn into fiction.

Historical candles do not show:

- spread blowouts

- partial fills

- worse-than-expected stop execution

- order rejection or delay

- the tendency to chase after the first spike

If your backtest assumes perfect entry and exit at candle prices during a violent release, it is probably overstating the edge.

Segment by event type, pair, and time of day

CPI is not NFP. NFP is not an FOMC decision. EUR/USD on U.S. data is not the same as GBP/USD around a Bank of England day or USD/JPY around the Bank of Japan decision.

Event-specific testing matters because reaction structure differs.

Measure what matters

If you want a useful journal or backtest, log:

- event type

- pair traded

- spread before release

- widest spread observed

- entry method

- slippage assumption

- maximum adverse excursion

- maximum favorable excursion

- time until tradable structure formed

- whether the best decision was to skip

That record is less exciting than a perfect screenshot. It is also far more useful.

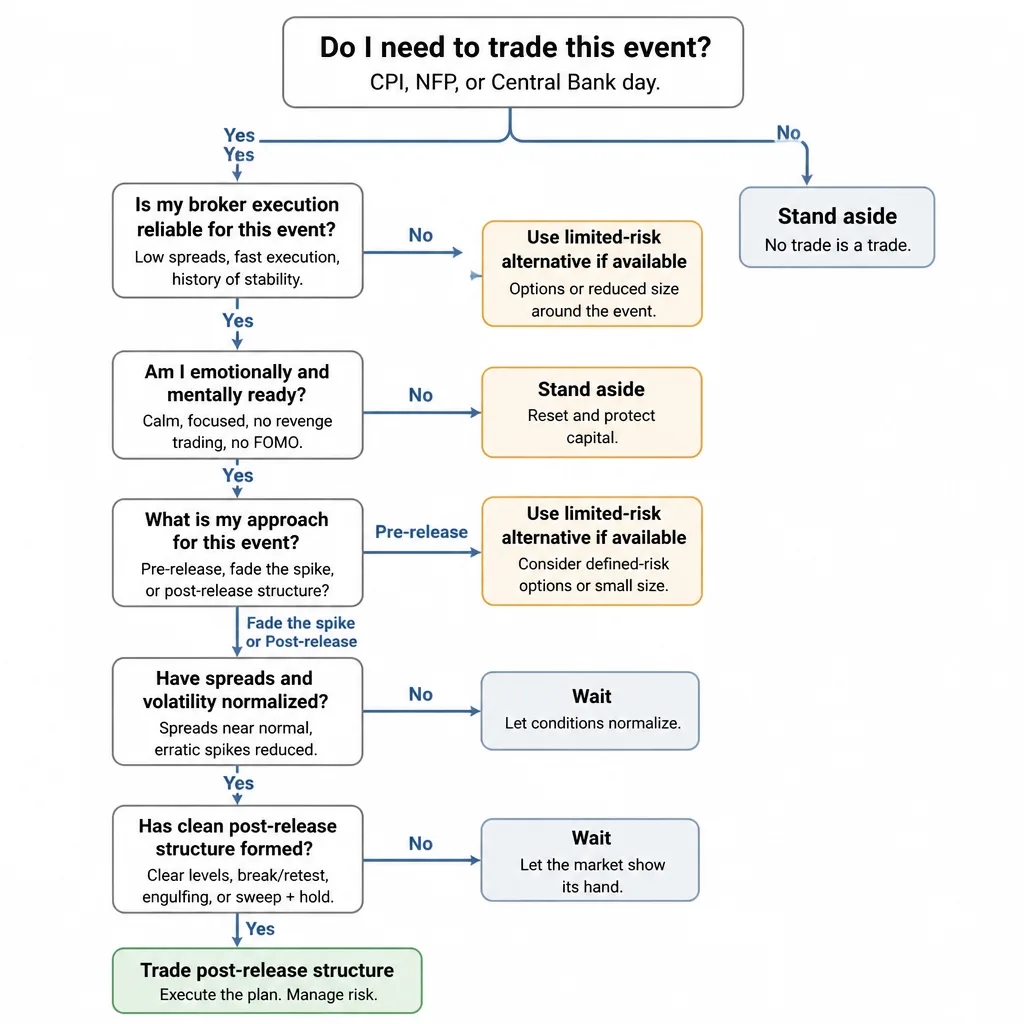

A simple news-day decision tree

Use this before every major release.

Do I need to trade this event?

- Is this event part of a tested plan?

- Do I understand what is being released and when? Use an economic calendar such as Forex Factory or Investing.com for scheduling, but remember that “high impact” is only a label, not a guarantee.[^6]

- Do I trust my broker’s execution during fast markets?

- Am I calm enough to wait?

If any answer is no, skip it.

If yes, which of the three approaches fits?

- Beginner or inconsistent execution? Stand aside.

- Discretionary trader with patience? Wait for post-release structure.

- Access to options or hedged alternatives and know how to use them? Consider a limited-risk alternative.

If structure is unclear, wait or walk away

After the release, ask:

- Have spreads normalized enough?

- Has the first chaotic repricing passed?

- Is there a clear range, retest, reclaim, or failed break?

- Can I define invalidation and size the trade sensibly?

If not, do nothing.

That is the playbook.

Conclusion

The biggest mistake on CPI, NFP, and central bank days is thinking the challenge is mainly directional. Usually it is structural.

News releases change the trading environment itself. Spreads widen. Fills degrade. The first move can mislead. A chart that looks obvious afterward may have been nearly untradeable in real time.

The better approach is blunt and effective: respect the release window, reduce size, stop treating the first spike as a gift, and trade only when post-news structure gives you something you can actually manage. On these days, the edge often belongs to the trader who can wait, not the one who can predict.

FAQ

Should you trade forex during CPI, NFP, or central bank announcements?

Not by default. For many retail traders, the safest choice is to stand aside unless they have a tested event-specific method, acceptable broker execution, and a clear plan for timing, size, and exits.

Why do traders get stopped out so easily during major news releases?

Because the problem is not just volatility. High-impact releases can widen spreads, increase slippage, create whipsaws, and thin liquidity enough to make normal stop placement far less reliable.

Can you be right on direction and still lose money?

Yes. A trader can read the macro surprise correctly and still lose if the entry is late, the stop sits inside release noise, or poor fills turn a planned loss into a larger one.

What usually changes in forex market conditions during CPI, NFP, and rate decisions?

Execution conditions often deteriorate. Traders commonly see wider spreads, slippage, skipped prices, sharp two-way sweeps, and delayed price discovery while the market digests the release and any revisions or guidance.

Is it better to avoid the first spike after a news release?

Often, yes. The initial move is frequently unstable and can reverse or extend once the market absorbs the details. Many traders are better served by waiting for post-release structure rather than chasing the first spike.

What is a practical pre-release no-trade window?

There is no universal rule, but many traders avoid opening fresh positions shortly before the release because spreads and liquidity can worsen even before the scheduled time. The key is to define the window in advance and test it.

What should traders watch in the first 1 to 5 minutes after the release?

Watch whether price is accepting direction or just printing chaotic two-way tails. Useful clues include narrowing spreads, fewer violent reversals, cleaner breaks that hold, and the emergence of a range or retest you can actually manage.

What is a safer way to stay involved?

A more defensible approach is to trade the post-release structure. That means waiting for a range, break-and-hold, reclaim, pullback, or failed breakout after the release window becomes more readable.

How should position size change on major news days?

Position size usually needs to be smaller because chart-based stop distance may understate real risk when spreads and slippage expand. If the setup requires a wider stop, size should typically be reduced to keep account risk controlled.

Why are pre-news highs and lows dangerous stop locations?

Those levels are often obvious to everyone, and major releases can sweep both sides before a clearer move forms. On news days, a technically logical stop can still be vulnerable if it sits inside unstable price discovery.

How do central bank days differ from CPI or NFP days?

Central bank days can unfold in stages. The rate decision may trigger one move, the statement another, and the press conference a third. That makes a single-timestamp trading plan less reliable than many traders assume.

How can you backtest a forex news trading strategy without fooling yourself?

Separate event days from normal days, segment by event type and pair, and avoid assuming perfect fills at candle prices. A more realistic test includes spread assumptions, slippage, skipped trades, and the time it takes for structure to form.