Most retail forex traders end up in one of two bad places with macro

They either ignore it and get blindsided by CPI, FOMC, or a Bank of England decision. Or they drown in headlines, read ten opinions, and still have no idea what to do when the number hits.

The answer is not to become a macro economist. It is to build a short weekly process that tells you three things: what could move your pairs, which price levels matter if it does, and what would make your idea wrong.

A good macro plan does not predict every move. It filters, frames, and prepares. Done well, macro stops being noise and starts becoming structure.

Why most retail traders either ignore macro or misuse it

The two common mistakes: avoidance and headline overload

The first mistake is simple: “I’m a technical trader, so I don’t need macro.”

That works until a clean setup gets steamrolled by U.S. CPI or an FOMC press conference. In FX, scheduled macro is not background noise. It can reprice interest-rate expectations, shift bond yields, and change how traders value a currency within minutes.[^1][^2]

The second mistake looks smarter than it usually is. A trader reads every alert, every social post, every hot take after a release. The result is information overload without a plan.

More macro reading does not automatically improve decisions. Often it just gives you more ways to justify an impulse.

What macro should do for a trader

For most retail traders, macro works best as a risk-framing tool, not a prediction tool.

That means knowing which events can realistically shift expectations, which pairs are exposed, and whether this is a week to press an idea, reduce size, or stay out. The edge is not in guessing the print. It is in knowing which print would matter and what price behavior would confirm it.

A couple of plain-English definitions help.

Rate expectations are what the market currently thinks a central bank is likely to do with interest rates over the next few meetings. Tools like the CME FedWatch Tool summarize this for the Fed.

Reaction function means what policymakers seem to care about most right now. Sometimes that is sticky inflation. At other times it is labor-market weakness, slowing growth, or tighter financial conditions. That focus changes, which is why the same CPI miss can matter a lot in one month and much less in another.[^2][^3]

Core thesis: a simple weekly process beats constant news consumption

Retail traders do not need a terminal full of economists’ notes.

They need a repeatable 30-minute routine that filters for expectation-shifting events and turns them into scenarios, levels, triggers, and invalidation. A simple process followed every week will beat random headline consumption almost every time.

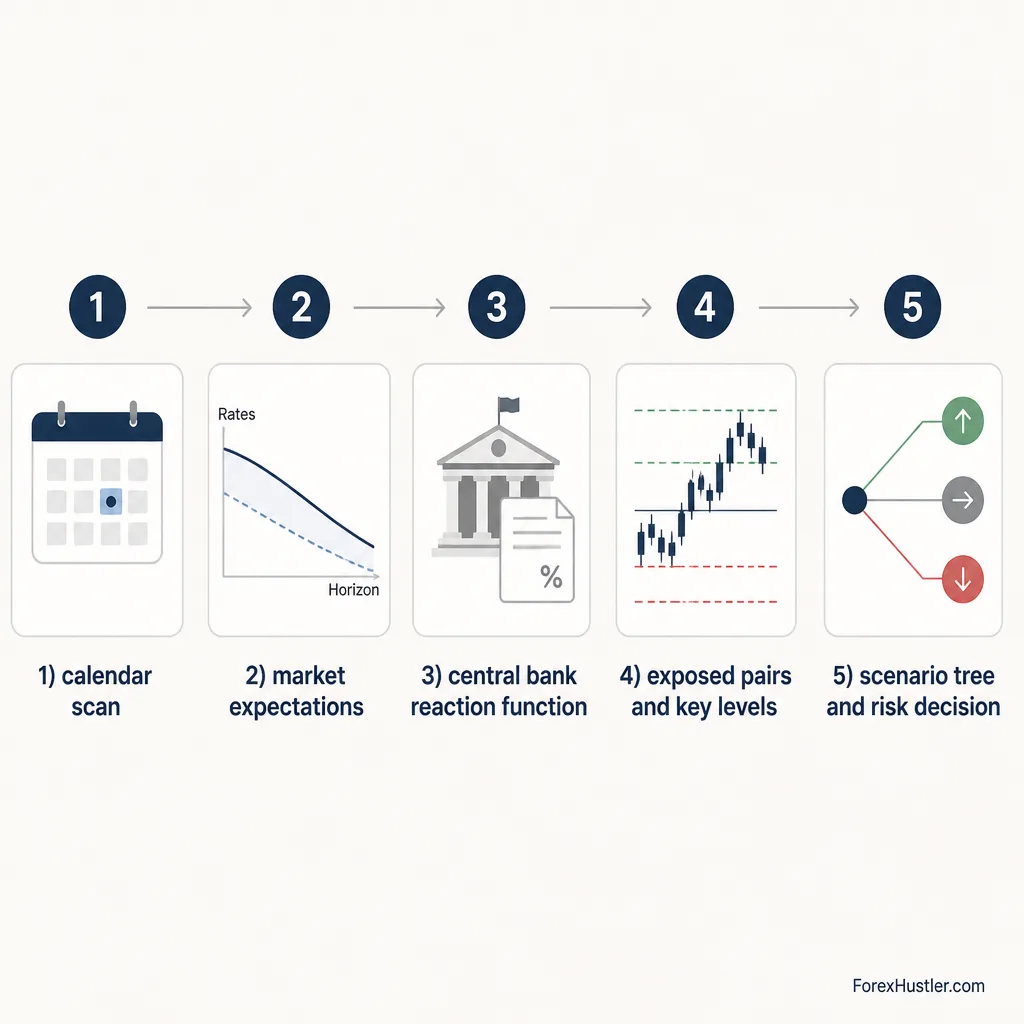

The 30-minute weekly macro routine

This needs to be realistic. If the routine takes two hours, most part-time traders will stop doing it.

A normal week might look like this:

- 5 minutes: scan the calendar

- 7 minutes: check market expectations

- 5 minutes: note the central bank reaction function

- 8 minutes: mark charts and exposed pairs

- 5 minutes: write scenario notes and risk decisions

Step 1: Start with the calendar and isolate the events that can reprice expectations

Use a scheduling tool like Forex Factory’s calendar or TradingEconomics to see what is coming. These are useful for timing, not analysis.

The question is not, “What is red folder this week?”

It is: Which events can actually change rates pricing?

Usually that means:

- inflation releases like U.S. CPI or UK CPI

- labor data like Nonfarm Payrolls or UK wage numbers

- central-bank decisions, statements, projections, minutes, and press conferences

- occasionally growth data when policy is finely balanced

A high-impact label is not enough. Some events create volatility without offering much tradable clarity.

Step 2: Check what the market already expects

The number itself matters less than the gap between the number and expectations.

Before U.S. CPI, for example, you want a rough sense of what the market is pricing for the next one or two Fed meetings. You do not need to model OIS curves yourself. You just need to know whether traders lean toward more cuts, fewer cuts, or no change.

For the Fed, start with the Federal Reserve for official policy materials, then use rates-market summaries like FedWatch for probability context. For the BoE, use the Bank of England’s monetary policy page.[^2][^3]

Step 3: Note the reaction function

This is where traders often overcomplicate things.

Ask one question: What is this central bank most sensitive to right now?

If the Fed is focused on sticky services inflation, CPI details matter more than the headline alone.[^4] If the BoE is worried about inflation persistence and wage pressure, UK CPI and labor data matter more than a second-tier growth print.[^3][^5]

One line in your notes is enough:

- Fed focus this week: inflation persistence and whether cuts can be delayed

- BoE focus this week: sticky inflation, wage growth, vote split, guidance on cuts

Step 4: Mark the pairs and sessions most exposed

Do not try to trade everything.

If the key event is U.S. CPI, focus on USD pairs like EUR/USD or USD/JPY. If the event is a BoE meeting or UK CPI, focus on GBP/USD or EUR/GBP.

Then note the session. A BoE release in London hours behaves differently from a U.S. inflation print heading into New York. Liquidity changes. So does the quality of follow-through.

Step 5: Build a short scenario tree before the week begins

This is the whole point of the routine.

You are not writing a forecast. You are building conditional branches:

- If the event is more hawkish than expected, what should happen?

- If it is more dovish than expected, what should happen?

- If it is mixed or in line, what does no-trade look like?

That gives you a map before the noise starts.

What to track each week and what to ignore

Track the releases that can shift rate expectations

Track the releases that can change policy expectations now, not in theory.

For the U.S., that often means CPI, Employment Situation reports, FOMC statements, projections, and Powell’s press conference.[^1][^2][^6]

For the UK, that often means ONS inflation data, labor-market releases, and BoE decisions, vote splits, and guidance.[^3][^5]

Track market pricing, not just the economic number

A hotter CPI print matters only if it changes what traders think the central bank will do next.

That is what repricing means in plain English: the market changes its view on future rates, yields move, and currency demand adjusts.

In FX, relative expectations matter. A hawkish Fed helps USD most clearly when it is more hawkish than what was priced, and more hawkish relative to other central banks.

Ignore low-value headlines and minor releases

A lot of macro content is commentary dressed up as signal.

You can ignore most of it.

You do not need every speech excerpt, every social-media reaction, or every minor release with little chance of changing policy expectations.

Ignore the urge to react to every alert in real time

Fast news trading is a different game.

Some professionals do make money trading the first few seconds after a release. Most retail traders do not have the speed, spreads, tools, or execution quality for that game. For them, being first is often worse than being late.

How to turn CPI, FOMC, and BoE into a tradable plan

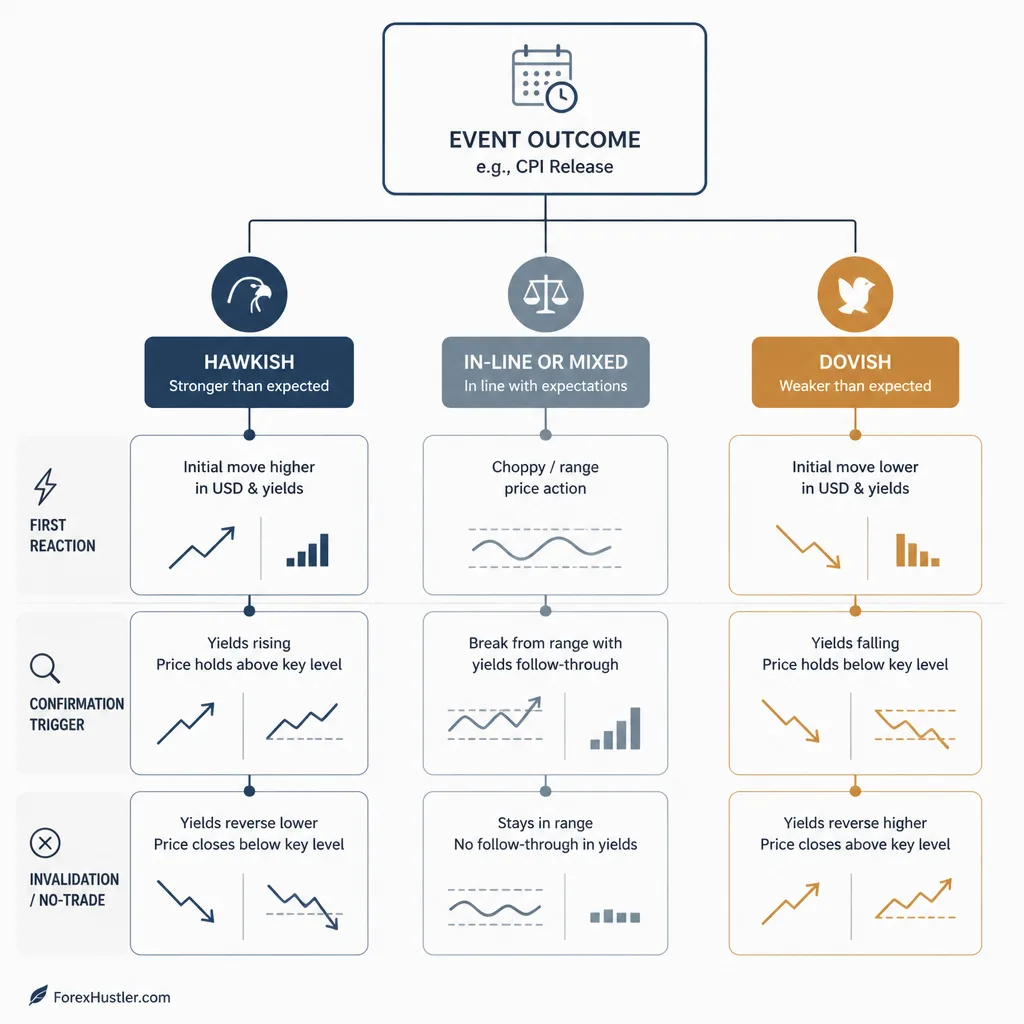

Translate event risk into scenarios: hawkish, neutral, dovish

Keep it simple.

For a U.S. CPI release:

- Hawkish: inflation runs hot enough to reduce expected Fed cuts

- Neutral: roughly in line, not enough to shift pricing much

- Dovish: soft enough to increase confidence in earlier or deeper cuts

For a BoE meeting:

- Hawkish: firmer inflation concern, tighter vote split, fewer cuts implied

- Neutral: policy and guidance broadly match expectations

- Dovish: softer tone, weaker inflation concern, more room for cuts

Add surprise magnitude

Not every surprise matters equally.

A tiny CPI beat may create a fast spike and then die. A larger surprise, especially with firm core details, is more likely to shift rate expectations in a meaningful way.[^1][^4]

The same logic applies to central banks. A hold is not always neutral. A hold with unexpectedly hawkish guidance can still move FX.

Separate the first reaction from durable follow-through

The first reaction is often an algorithmic burst.

The more useful question is what happens after that. Does EUR/USD break the pre-event low and stay below it? Does USD/JPY clear a prior swing high and hold? Do yields confirm the move, or do they fade quickly?

If a move cannot hold key levels, that often tells you the headline was not enough.

Pre-mark the levels that matter

Before the event, mark levels that matter:

- prior day high and low

- prior week high and low

- Asian or London range

- pre-event range

- obvious swing highs and lows

- round numbers

- zones where price previously spent meaningful time trading

That last one is what traders often mean by an acceptance area. It is a place where price did not instantly reject value.

Technicals tell you where the market may react. Macro tells you why this week might be different.

A simple scenario tree you can use every week

Here is a compact example for U.S. CPI using EUR/USD.

If the result is more hawkish than expected

Suppose CPI comes in materially hotter than consensus and the details are firm enough to reduce expected Fed cuts.

Your trigger is not “CPI hot, buy USD.”

It might be:

- hotter CPI

- Treasury yields push higher

- EUR/USD breaks below the pre-event range low and holds below it for several minutes

Only then do you look for an entry, maybe on a failed retest of that broken level.

If the result is more dovish than expected

If CPI is soft and rate-cut expectations rise, USD may weaken.

Now your trigger could be:

- softer CPI

- yields fade

- EUR/USD reclaims the pre-event high and accepts above it

Again, the entry comes after the trigger. They are not the same thing.

If the release is mixed or close to expectations

This matters more than many traders admit.

If CPI is near consensus, details are mixed, and EUR/USD stays trapped inside the pre-event range, there may be information but no trade. That is a valid outcome.

No-trade is part of the plan, not a failure of the plan.

Define triggers and invalidation without predicting direction

A trigger is the condition that makes the setup worth watching.

An entry is your actual execution after price confirms structure.

An invalidation is what proves your idea is wrong. For a bullish USD idea, that might be:

- price snaps back into the pre-event range

- the breakout level fails immediately

- yields stop confirming the move

That is cleaner than trying to predict direction before the event.

Using the calendar as a risk tool, not a signal generator

When to reduce size, stay flat, or wait

For many retail traders, the calendar is at least as useful for avoiding bad timing as it is for finding good timing.

If you cannot watch CPI, FOMC, or a BoE decision live, holding full-size exposure through it is often unnecessary risk. Reducing size, taking partial profits, or staying flat is often the better choice.

Why spreads, slippage, and liquidity matter

Around major releases, spreads can widen sharply and stop orders can fill worse than expected. That means a setup that looks attractive on a chart may behave very differently in real execution.

That is one reason post-release structure is often safer than pre-release guessing.

Do not force a trade just because an event is scheduled

A scheduled event is not an obligation.

Some events create real opportunity. Others are mainly warnings not to be poorly positioned. Those are not the same thing.

Why markets sometimes fade the news

Expectations were already priced in

A hawkish outcome can still fail if traders had already moved aggressively into that view.

If USD rallied for several sessions before CPI and yields had already repriced, a hot print might not have much fresh fuel left.

Positioning was crowded

You do not need perfect positioning data to sense this. Sometimes the market is obviously leaning one way.

A one-way run into the event often means the easy move may already have happened. CFTC Commitment of Traders data can help with broader context, though it is delayed.[^7]

The headline looked strong, but the details were soft

This happens constantly with inflation data.

A headline may beat, but core details, revisions, or services components may weaken the interpretation. Markets do not trade headlines in isolation for long.[^1][^4]

Broader flows overpowered the macro signal

Sometimes the macro story is clear, but broader risk-on or risk-off flows dominate anyway.

That is why “good news strengthens the currency” is too crude to trade well.

Common failure modes in weekly macro planning

Confusing economic direction with currency direction

Strong data does not automatically mean a stronger currency.

The real question is whether the data changes policy expectations, and whether that change matters relative to what was already priced.

Using macro to justify a technical bias

This is one of the easiest traps.

If you already wanted to short EUR/USD, macro can become a storytelling device instead of a decision tool. The plan should test your bias, not decorate it.

Ignoring timing, liquidity, and positioning

A solid macro view can still fail if you apply it in the wrong session, in poor liquidity, or into a crowded market.

Treating every high-impact event as tradable

Some releases matter. Some only create noise. Some matter but still do not produce a clean setup.

That distinction is part of the job.

A one-page weekly template for forex traders

Use this in your journal or notes app:

| Field | What to write |

|---|---|

| Event | U.S. CPI, FOMC, BoE, UK CPI, NFP |

| Current expectation | What the market broadly expects for the next 1–2 meetings |

| Why it matters now | Inflation focus, labor weakness, growth concern, vote split risk |

| Hawkish scenario | What outcome would reduce expected cuts or raise yields |

| Dovish scenario | What outcome would increase expected cuts or soften policy tone |

| No-trade scenario | In-line or mixed result with price stuck in range |

| Key levels | Prior day/week high-low, pre-event range, round numbers, swing levels |

| Trade trigger | Event outcome plus level hold or acceptance |

| Invalidation | Return into range, failed breakout, yields not confirming |

| Risk decision | Trade, reduce, stand aside, or wait for post-release structure |

A practical GBP example might look like this:

- Event: BoE decision

- Expectation: Hold expected, modest cuts priced later

- Why it matters now: Market sensitive to guidance and vote split

- Hawkish scenario: Hold plus firmer inflation concern and less dovish guidance

- Pair: GBP/USD or EUR/GBP

- Key levels: Prior week high in GBP/USD, prior week low in EUR/GBP

- Trigger: GBP/USD breaks and holds above prior week high after statement and conference tone confirms

- Invalidation: Fast rejection back below the breakout zone

That is enough. It is clear, tradable, and falsifiable.

The real goal of macro prep

You are not trying to forecast every move

That is where many traders waste energy.

A weekly macro plan is not about knowing the future. It is about knowing what would matter if it happens.

You are trying to know what would change your view

That is the deeper edge.

When you define the trigger and invalidation before the event, you stop inventing stories after the fact.

Good macro prep creates fewer, cleaner decisions

That is what good preparation feels like.

Not more opinions. Not more alerts. Fewer decisions, made with better context.

Conclusion

Macro becomes useful when you stop treating it like prophecy.

You do not need to predict CPI, decode every FOMC adjective, or read every BoE headline in real time. You need a short routine that filters for the events with real repricing power, checks what the market already expects, marks the levels that matter, and defines what would confirm or invalidate the trade.

That is the real value of macro prep in forex. It does not make you certain. It makes you organized.

And in a market that punishes impulsive decisions, organized is a real edge.

FAQ

What is a weekly macro plan in forex trading?

A weekly macro plan is a short preparation process that helps you identify which economic events can move your pairs, what the market expects, which levels matter, and what would confirm or invalidate a trade idea.

Do I need to predict the CPI or FOMC outcome to trade macro in forex?

No. The goal is not to predict the number. The goal is to prepare scenarios in advance so you know what matters, which pairs are exposed, and what price behavior would make the setup tradable.

Which macro events matter most for retail forex traders?

Usually the highest-value events are those that can shift rate expectations: inflation data, labor-market releases, central bank decisions, policy statements, press conferences, and sometimes growth data when policy is finely balanced.

What do rate expectations mean in plain English?

Rate expectations are the market’s current view of what a central bank is likely to do with interest rates over the next few meetings. Forex often reacts more to changes in those expectations than to the headline data alone.

What is a central bank reaction function?

A reaction function is what policymakers seem to care about most at the moment. That could be sticky inflation, weakening jobs data, slowing growth, or financial stress. It helps traders judge which data points are most likely to matter now.

How do I turn CPI, FOMC, or BoE into a tradable forex plan?

Start with current expectations, then build a simple scenario tree: hawkish, in line, or dovish. Next, mark key levels on the chart, define the event trigger, and decide what price action would invalidate the idea.

What levels should I mark before a major forex news event?

Useful pre-event levels include the prior day high and low, prior week high and low, the pre-event range, session highs and lows, round numbers, obvious swing points, and areas where price previously accepted or rejected value.

What is the difference between a trigger and an entry in news trading?

A trigger is the condition that makes the setup worth watching, such as a hotter-than-expected CPI print and a hold above a key level. An entry is the actual execution after price confirms structure, acceptance, or momentum.

Why does forex sometimes move opposite to the news headline?

Because the headline is only part of the story. The move may already be priced in, positioning may be crowded, underlying details may be weaker than the headline, or broader risk sentiment and yields may be driving the market instead.

Should I trade every high-impact event on the economic calendar?

No. High-impact does not automatically mean a high-quality setup. Many events are more useful as risk markers that tell you when to reduce size, stay flat, or wait for post-release structure.

How should part-time forex traders handle CPI, FOMC, or BoE releases?

If you cannot monitor the release and the first few minutes after it, reducing size or standing aside is often more rational than holding full exposure through unpredictable spreads, slippage, and fast price swings.

How long should a weekly macro routine take?

For most retail traders, about 30 minutes is enough in a normal week: scan the calendar, check expectations, note the central bank reaction function, mark exposed pairs and levels, and write a few scenario notes.